Energy Transition #5: India - Opportunities Galore: Mapping the whole Ecosystem (Part 1)

Energy Transition #5: India - Opportunities Galore: Mapping the whole Ecosystem (Part 1)

Energy Transition: India Deep Dive (Part 1)

If you haven’t checked it out yet, I’ve covered the overview of Electrification theme in my previous post:

The feedback I’ve got on this post is to cover the companies present in the ecosystem. So I’ll attempt to map the ecosystem. However, this is a dynamic field so your feedback will be paramount for updating this post to stay relevant.

Before I start dissecting the sector, let’s look at the opportunity size:

(1) 500GW of Renewable Energy by 2030

Roughly 200GW has been installed by the end of FY2024 (Including Hydro) i.e. ~300GW to be installed in the next 6 years translating to an average of 50GW / Year (40 Solar and 10 Wind). If we roughly assume a cost of 1MW Solar around 3 crore INR and 1MW wind approx 4.5 crore, the market size is approx 10 Lakh Crore

(2) NEP has already projected investments of 4.75 Lakh Crore in power transmission

“Capital is attracted into high return businesses and leaves when returns fall below the cost of capital” - Capital Returns by Edward Chancellor

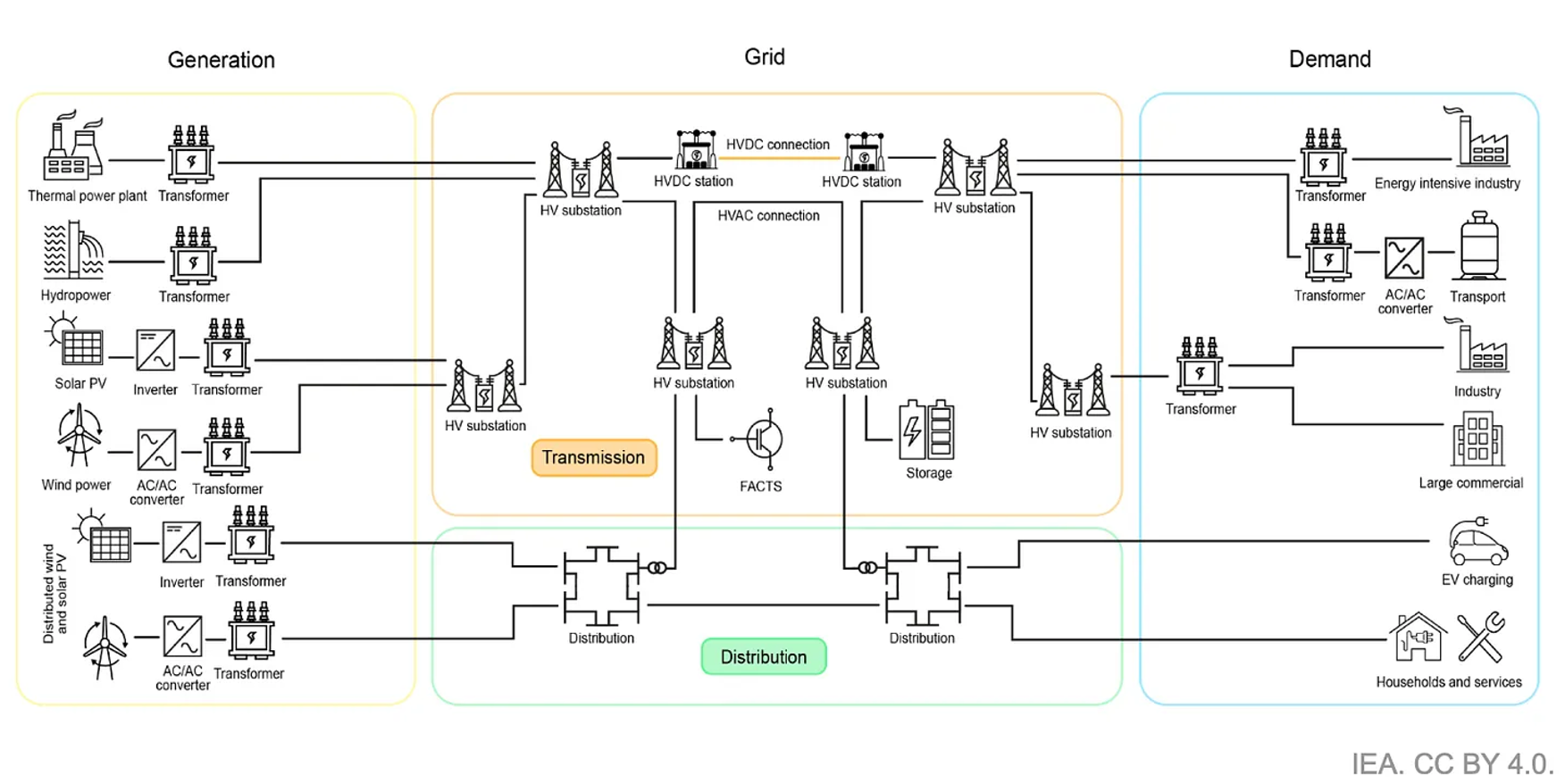

With this backdrop, let’s deep dive into the Indian Power Sector and map the companies present in the Value Chain

Generation

1. Solar Module Manufacturers

Module accounts for approx 60% of the cost. However, it is the riskiest part of the value chain with fierce competition.

Currently, the regulatory environment is favorable with ALMM and BCD. There are over 80 companies in the ALMM list plus some global players are also active in the market. Looking at the supply side the enlisted capacity is 37.6GW which is further expanding. In the near term, the indications are installations of 50 GW of renewables (including solar and wind). We are accordingly approaching the country’s requirements. Further capacity additions may either increase the pace of solar installation or lead to a glut if the supply can't be absorbed.

In the past, solar additions across the globe have surpassed expectations but remember the growth in solar has to be equally augmented with transmission without which we may build capacity only waiting to be connected to the grid.

Let's think from the Government's Perspective on regulations

The regulations could have been loose to benefit from lower module prices which could have spurred further growth in Solar installations. Though this is good for the short term, we could have been exposed to an even more global risk in the long term. With the ALMM and BCD, one the govt now has a lever in controlling the prices and secondly, it helps build capacity in our own country. Remember the regulations and duties are not set in stone, this is a dynamic process. If the environment changes, so do the policies.

Hasn't the same played out in petrol/diesel? Instead of exposing the end user completely to global markets, the excise is now a lever in the hands of the govt, providing some bandwidth for price control.

Regulation will be a key risk. Why should the government let someone make a supernormal return?? 💡

This has played out in Sugar. It has played out in the form of windfall tax in the Oil Sector.The complete list of ALMM can be accessed here.

Some prominent names are:

Mundra Solar (Adani), Tata Solar, Jackson Engineers, Vikram Solar, Waaree Energies, ReNew, Premier Energies, Renewsys India, Goldi Solar, Emmvee, Genus Innovation and BHEL etc.

Some of the listed players are- Insolation Energy, Solex, Alpex Solar, Swelect, Websol, etc.

Since last year there was no ALMM requirement the leader of the pack was not an Indian Company but was Jinko Solar.

The pace of technology change is fast. Here technology upgrade is the maintenance capex.

I'm biased against investing in companies that solely rely on ALMM for their survival. The pace of change is fast and the companies may not be able to pivot towards new technologies time and again. This is a commoditized business more or less.On the positive side if Indian exports get preference or get competitive then the module manufacturers will further prosper.2. Wind Turbine manufacturers

Similar to module manufacturing, the key component in Wind is the turbine. However, the pace of technology change is less compared to Solar Modules.

versus time with the 1990 0.2-MW turbine tower stands 30 m tall with a rotor diameter of 30; the 2000 0.9-MW turbine stands 58 m tall with a 53-m rotor diameter; the 2010 1.8-MW turbine stands 80 m tall with an 84-m rotor diameter; the 2020 3-MW turbine stands 90 m tall with a 125-m rotor diameter; the Washington monument stands 169 m tall; and a 3-MW turbine labeled “Innovations Turbine” stands at 160 m tall with a 150-m rotor diameter.")

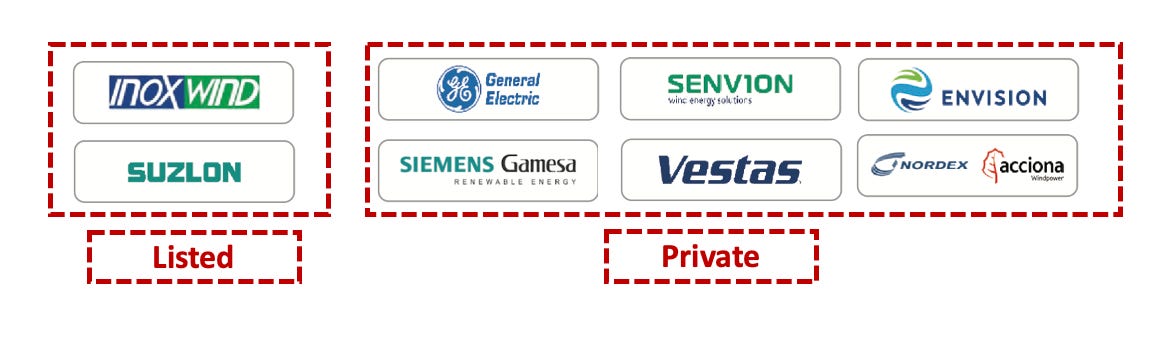

Some of the players in the Wind Energy Sector are:

RLMM regulations: Non-tariff barrier. Around 30 models feature on the RLMM list. This space is much less crowded as compared to the solar space.

As per MNRE, there exists a manufacturing base of 15GW i.e. enough supply to realize the annual target of 10GW. The challenge here is not of supply rather execution is a challenge.

This has been aptly captured by Rahul in his Inox Wind Analysis where Inox has fallen short of expectations and Suzlon is citing challenges in execution

3. Engineering, Procurement, and Construction (EPC)

Think of them as the go-to guys for your project. These companies or this part of the business is the project execution business.

Starting from feasibility studies and designing, the EPC player is instrumental in the commissioning of the project.

The keyword in EPC business is Execution. Here the EPC players take on the risk of implementing the project.

Recipe for success: Technical know-how, financial prudence, and prudent bidding. Ultimately you will start moving up the value chain.

Typically one can expect 7-12 % EBITDA margins in this business. They don't have the technology obsolesce risk but rather have to manage the different aspects of the project.

Some of the key risks are also indemnified in the contract for example if the project owner is unable to provide land, etc.Credentials play an important role, once a company has executed a project of a certain size, it becomes easy for them to bag more contracts of higher capacity. Also moving up the size game in EPC requires balance sheet strength.

Side Note: Previous post on Waaree’s EPC Arm

Waaree Renewables Technologies Ltd

Some of the prominent players in the EPC are:

Please comment other significant players that I may have missed

New Trends

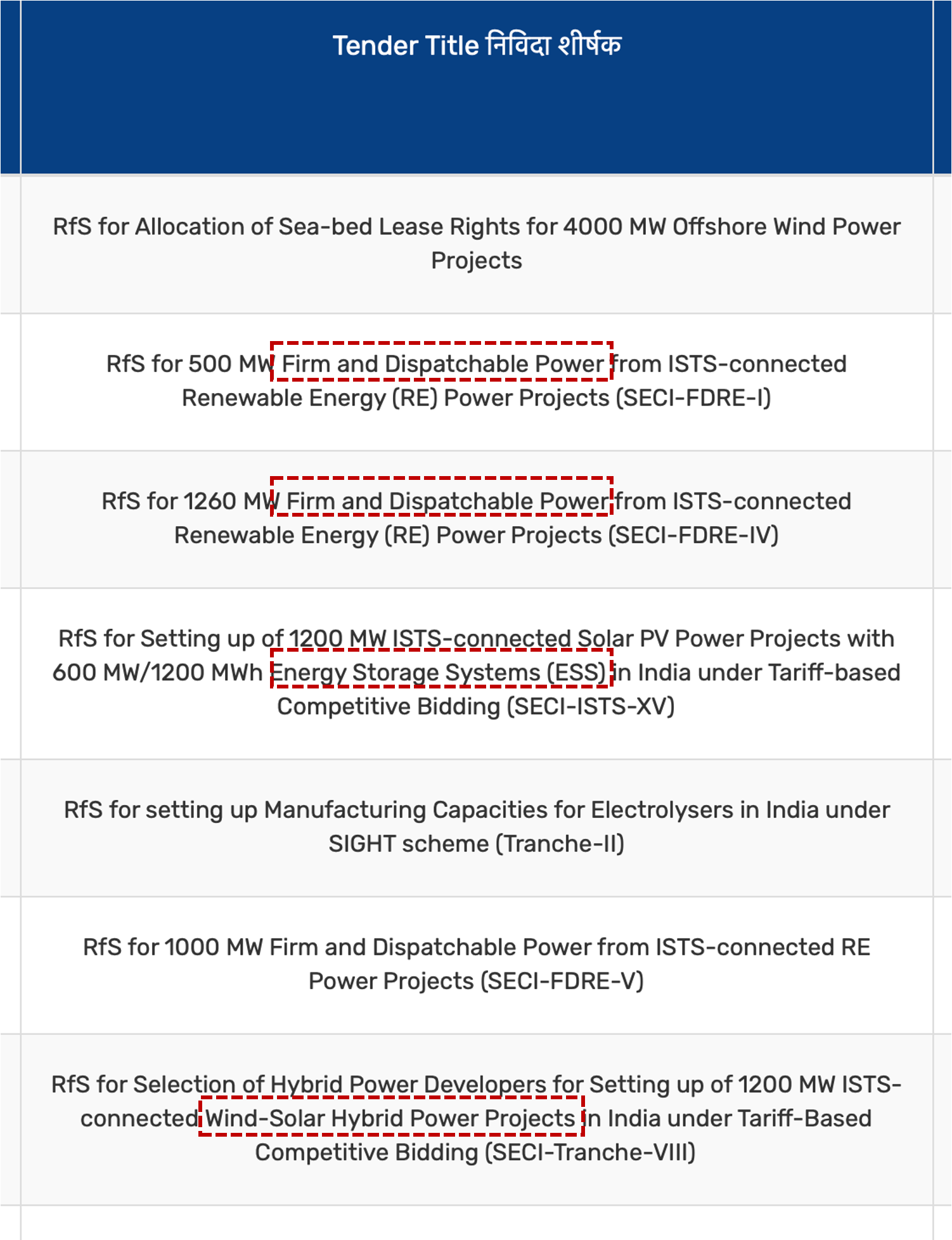

Change is the nature of the game. If you don’t grow with increasing requirements then you will be obsolete. The tenders issued tell the story. There is a pivot towards hybrid RE commissioning either Solar + Wind or combining BESS with this.

Conclusion

To invest just based on opportunity size only will lead to hard lessons. Capital cycles are real. As far as the manufacturing capacity of Solar Modules and Wind Turbines is concerned, we are not far from an oversupplied market. In an oversupplied market, in commodities, the only way prices go is downward.

The players may be saved from outside threats by the government but not from domestic competition.To me EPC players appeal - they can have operating leverage when large-size projects are executed. Always keep an eye on execution. Without execution no matter the size of the order book, you will be executed.

A gentle reminder of what can go wrong (More apt will be Suzlon in past cycle):

PS: Covering the whole sector in one post is a daunting task. So stay tuned for further thoughts on this Multi-Mega Theme. 😀

*****

Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

A comprehensive analysis of the sector provides valuable insights.Nice to read this Pankaj Ji

👍👍👍👍