Waaree Renewables Technologies Ltd

Waaree Renewables Technologies Ltd

Riding the Solar Wave

To say that Solar energy is witnessing significant growth in India and worldwide would be an understatement. On the face of it, we may line up multiple factors like impetus towards tackling climate change, government policies, net carbon neutral targets, energy independence, technological advantages, etc. These are enablers of energy transition but still in my opinion, the key factor why Solar is the leading solution among clean technologies is the unit economics - the highest potential at the lowest cost and the most decentralized solution.

Let’s sink this into our minds:

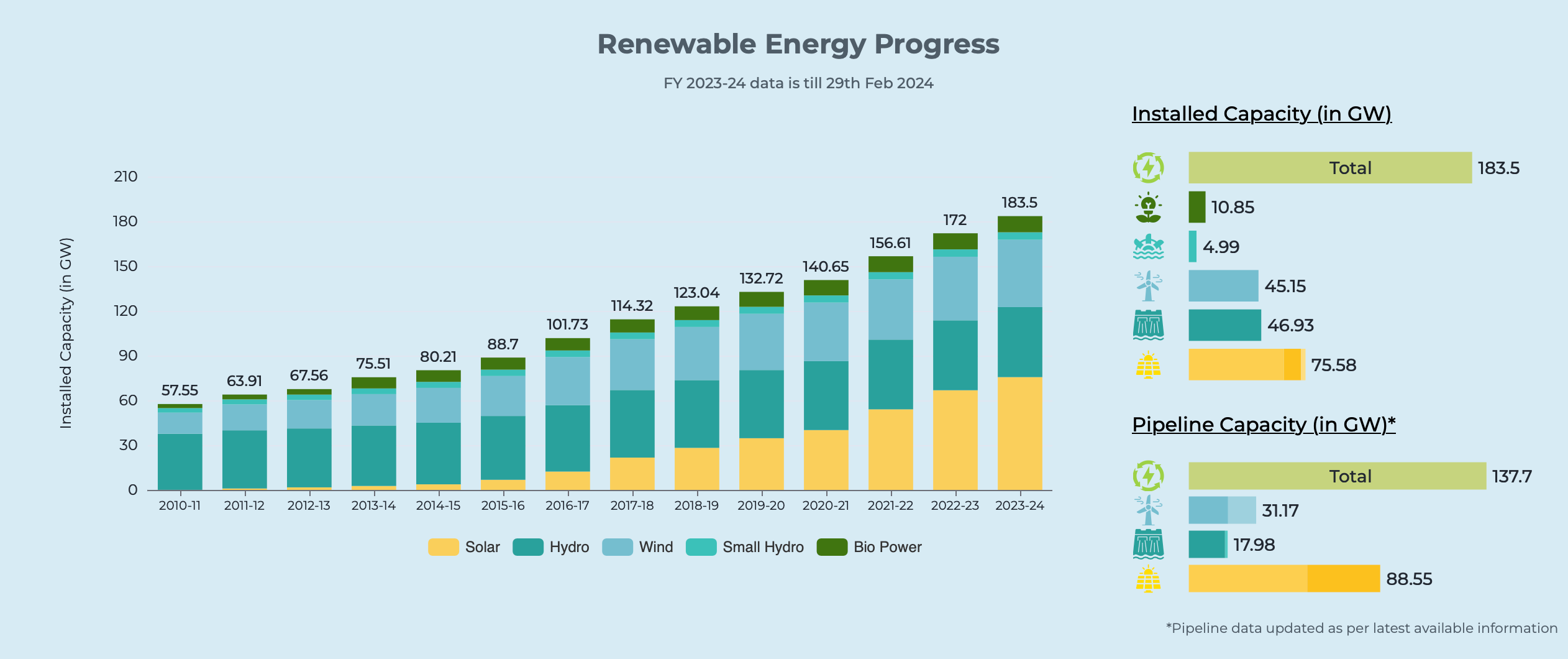

What Nuclear energy had achieved in 40 years (1965-2005), Wind + Solar has surpassed that in 20 years.

The growth in Solar capacity has been so explosive, that even the IEA (International Energy Agency) has continuously failed to estimate the pace of growth in Solar.

India has added 75.5 GW of solar since 2010 making Solar Energy the largest in the renewable energy mix (60% of renewable energy). More than the current installed capacity is already in the pipeline.

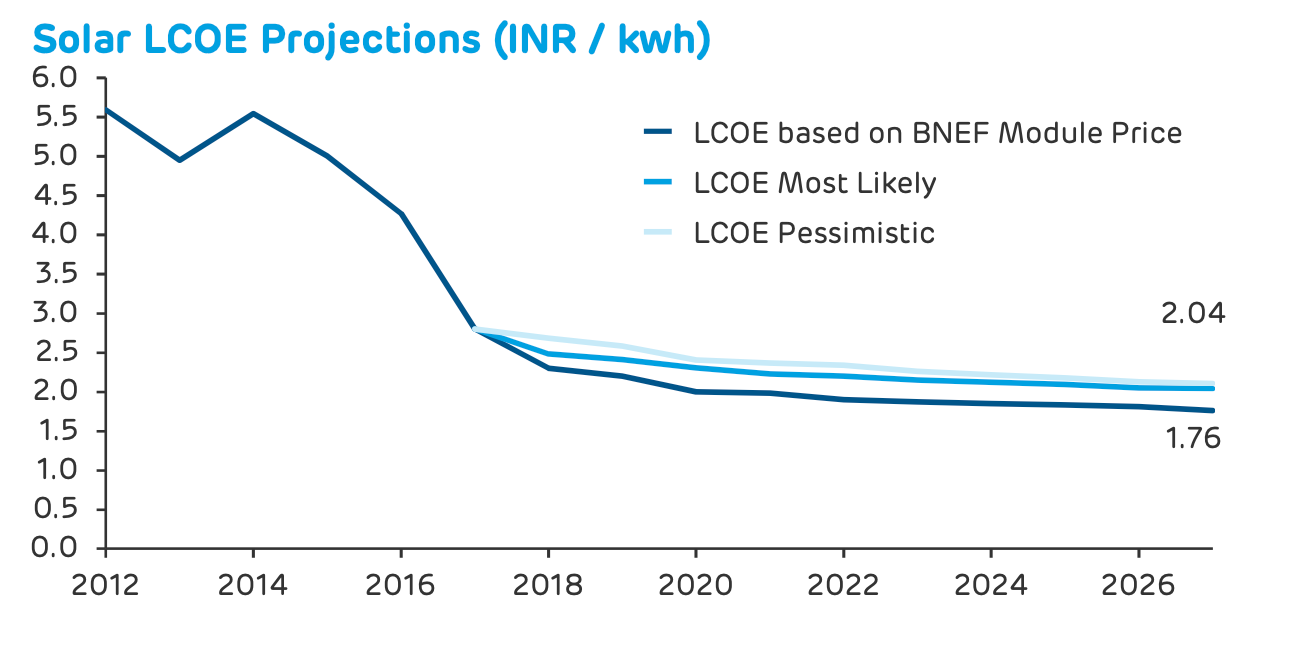

The Levelized Cost of Energy in Solar (LCOE: average net present cost of electricity generation for a generator over its lifetime) is becoming even more compelling.

Waaree Group at a Glace

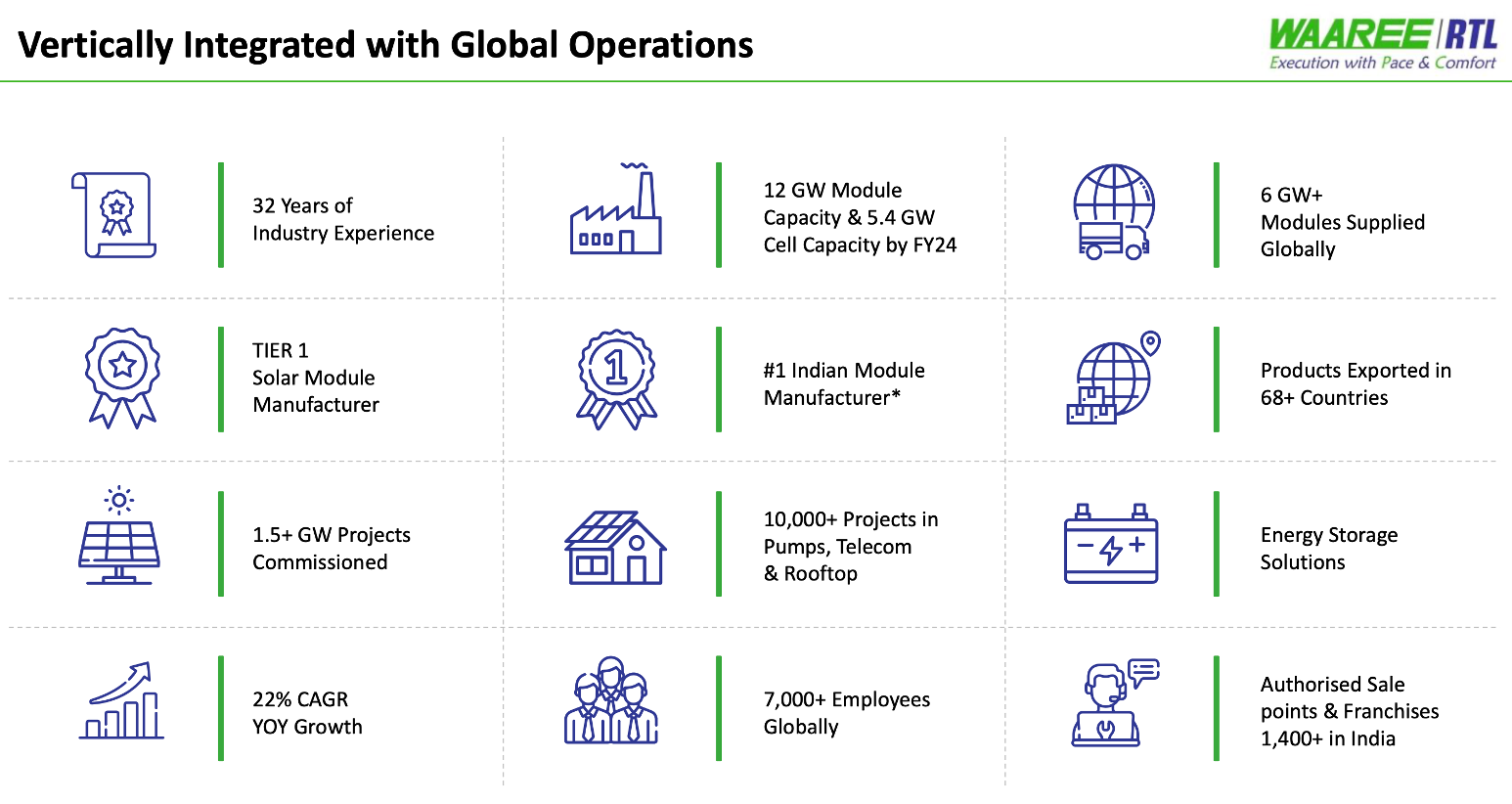

The group is present in renewable space. It has end-to-end capabilities in Solar Energy. The main company of the group is Waaree Energies Ltd. (WEL), which with its subsidiaries executes in different areas in the Solar Ecosystem.

The different Waaree Group companies and its business is as follows:

Waaree Energies Ltd. (WEL) - Parent Company - Engaged in manufacturing of Solar Modules - Not Listed; filed for IPO

Waaree Technologies Ltd - Subsidiary of WEL - In Energy Storage Solutions - Listed

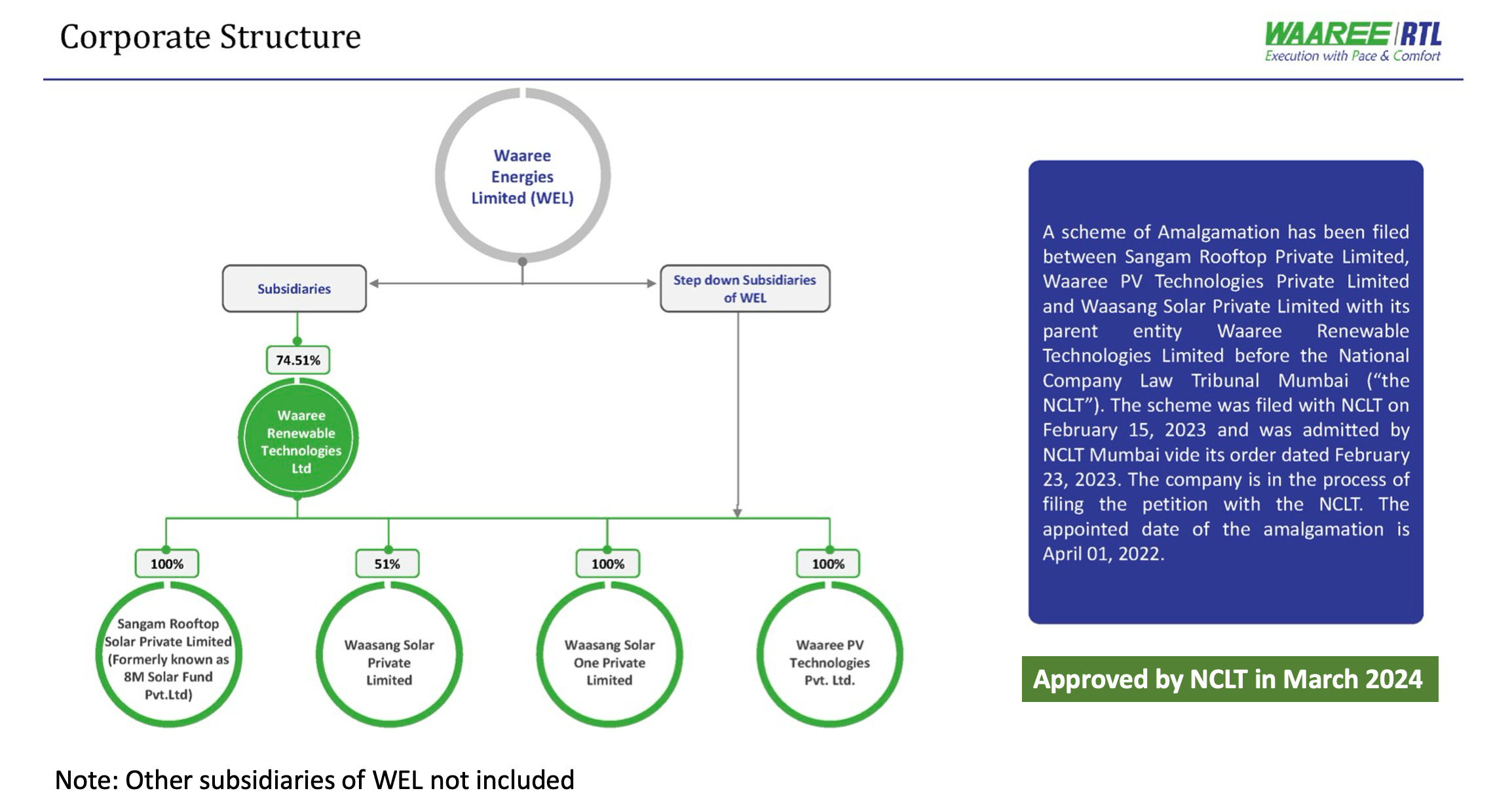

Waaree Renewables Technologies Ltd - Subsidiary of WEL - In Solar EPC Business - Listed

Waaree Renewables Technologies Ltd

Separately listed, EPC (Engineering, Procurement and Construction) arm of the Waaree Group.

Other segments include the IPP i.e. Independent Power Producer (finance, construct, own, and operate solar projects) and O&M (Operations & Maintenance).

Incorporated initially as Sangam Advisor providing financial services and listed on SME Platform in August 2012. Changed the name to Sangam Renewable Limited in May 2018. Again name was changed to the present name i.e. Waaree Renewable Technologies Limited in July '21.

Serve individual, industrial, and commercial customers, promoting energy solutions that reduce carbon emissions. Solutions/projects include on-site solar projects (rooftop and ground-mounted) and off-site solar farms (open-access solar plants).

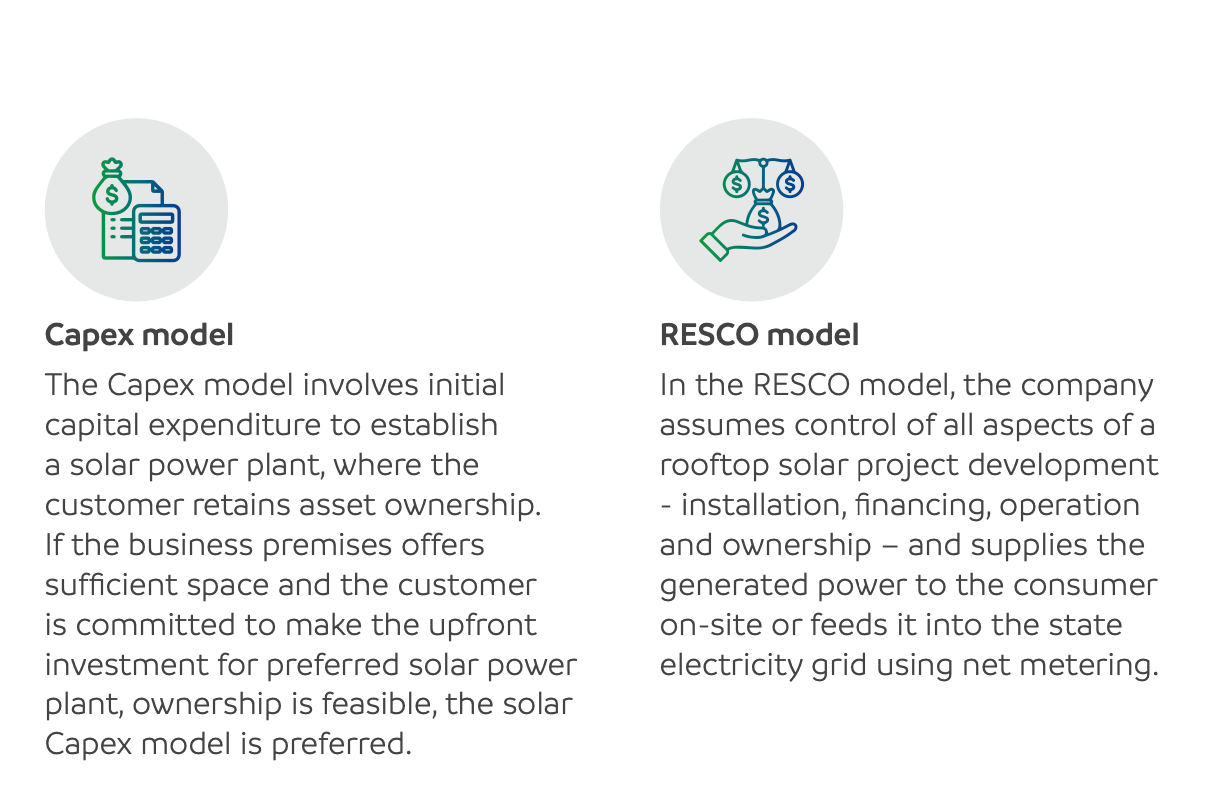

Capex model and RESCO Model

Business Segments

EPC (Engineering, Procurement and Construction)

Operations & Maintenance

Over 900+ MWp O&M Portfolio of solar power plant assets

Leveraging tech-based data analytics, technical audits, consulting, and R&D to improve overall plant efficiency and provide end-to-end solutions for all kinds of solar plants to reduce breakdown and maximize generation.

Plant remote Monitoring to observe plant real-time data and immediate response if any breakdown results to achieve maximum up-time Provide solutions to reduce downtime and maximize generation.

IPP (Independent Power Producer)

It is asset heavy business.

“Doing some of the projects where we see there is a good margin available and a good IRR available. Not intending to do much of the project on the company’s balance sheet.”

Better if the company keeps this segment on hold given the capital required.Green Hydrogen

Pilot Project: Secured contract for 1 MW Green Hydrogen Plant with an integrated ecosystem

“ There's a huge opportunity. I think all we need to do is scale up and acquire the required skill set to scale onto this business and we strive to do that. Hence, we have taken up this pilot project also. So very, very large pie. There are a lot many people, entities who are intending to go ahead. Whomever can scale up early and fast could be one of the early in the line.”

At this stage, this is a moonshot. Till the company exhibits some progress in this business, as an investor we should focus on the solar part of the story and be open about how the hydrogen space evolves for the company Business Strategy / Growth Strategy

Targets the commercial and industrial customer segments.

Tailwinds in this segment are driven by cost savings via lower electricity expenses, carbon credits, meeting ESG norms as well as other regulatory push/incentives. Especially, industries geared towards exports have to meet ESG norms to qualify for business in developed countries.

Business is skewed towards private projects rather than government projects. Around 85-90% of the projects are from the private side.

Aim to tap the growing renewable market, not only solar but Solar+Storage, Solar + Wind (no project yet), Hydrogen (got a pilot project but execution to be seen)

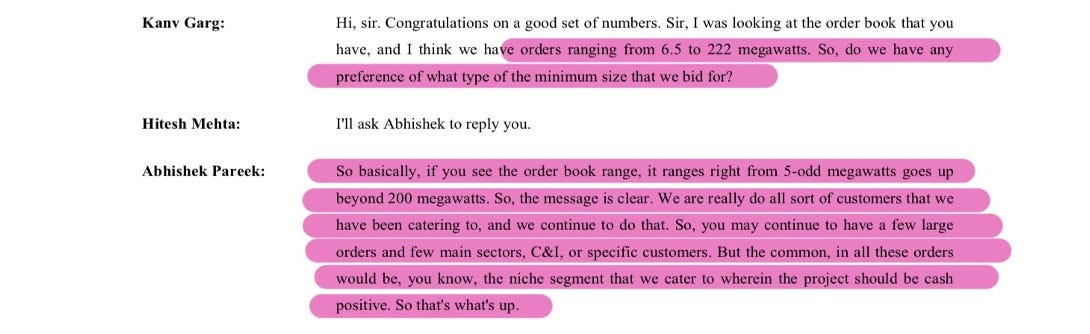

Focus is to get projects in all size categories from 5MW to 200 MW + based on its profitability

International Foray

Scaling Up

As per management they have an order pipeline of 9GW of which they expect to convert 30-40% of this pipeline i.e. an opportunity of around 3GW.

Management expects that India will add 40 GW of solar energy capacity each year spanning from fiscal year 2024 through fiscal year 2028, emphasizing a multi-year dedication to the growth of solar installations.

They are confident on scaling up as well.

Provide Value to Customers:

“We believe that it would be limiting to merely commission EPC projects on time. Our objective is to commission, schedule and design our solar infrastructure in a manner that our customers get the benefit of the highest yield, shortening their project payback.By catalyzing their generation yield (and hence cash flows), we seek to provide our customers with a greater incentive to reinvest by commissioning additional capacity, enhancing our revenue visibility.”

Risk Management

“We are very cautious while bidding also. And we are very selective in the kind of customers and the kind of projects and risk that we take. So, this is our appetite of a business. We really will try to limit our risk exposures. And we're not very keen to take on very, very high risky projects.”

Understanding Unit Economics

The major cost component of a Solar project is the cost of the Module which accounts for approx. 60%-65% of the project cost. With a module, the per MW cost is around 3.5 to 4 crore while without a module the cost is 1.25 - 1.50 Crore. Mostly 60-70% of the order book is without modules.

The execution period depends on the size of the project which has different unit economics.

For a smaller project like 10 MW the overall turnaround of a project is between one to two months and hence the exposure to the commodity price and other risk is limited and being a retail supplier, that leaves some more edge for a little bit higher margin.

On larger projects i.e. 200 megawatts plus size, it's more of a kind of supply chain management strength that enables the profitability of any project of a large-scale size, which is between 12 months to 15 months.

The business is not seasonal as execution keeps on happening throughout the year but the revenues are lumpy. Two factors contribute to it:

Dependence on commodity prices

The nature of the business and the revenue recognition

EBITDA margins overall are expected to be in the range of 15% to 20% as per management. However, given the tilt towards larger projects, the conservative estimate should be 10%-15%.

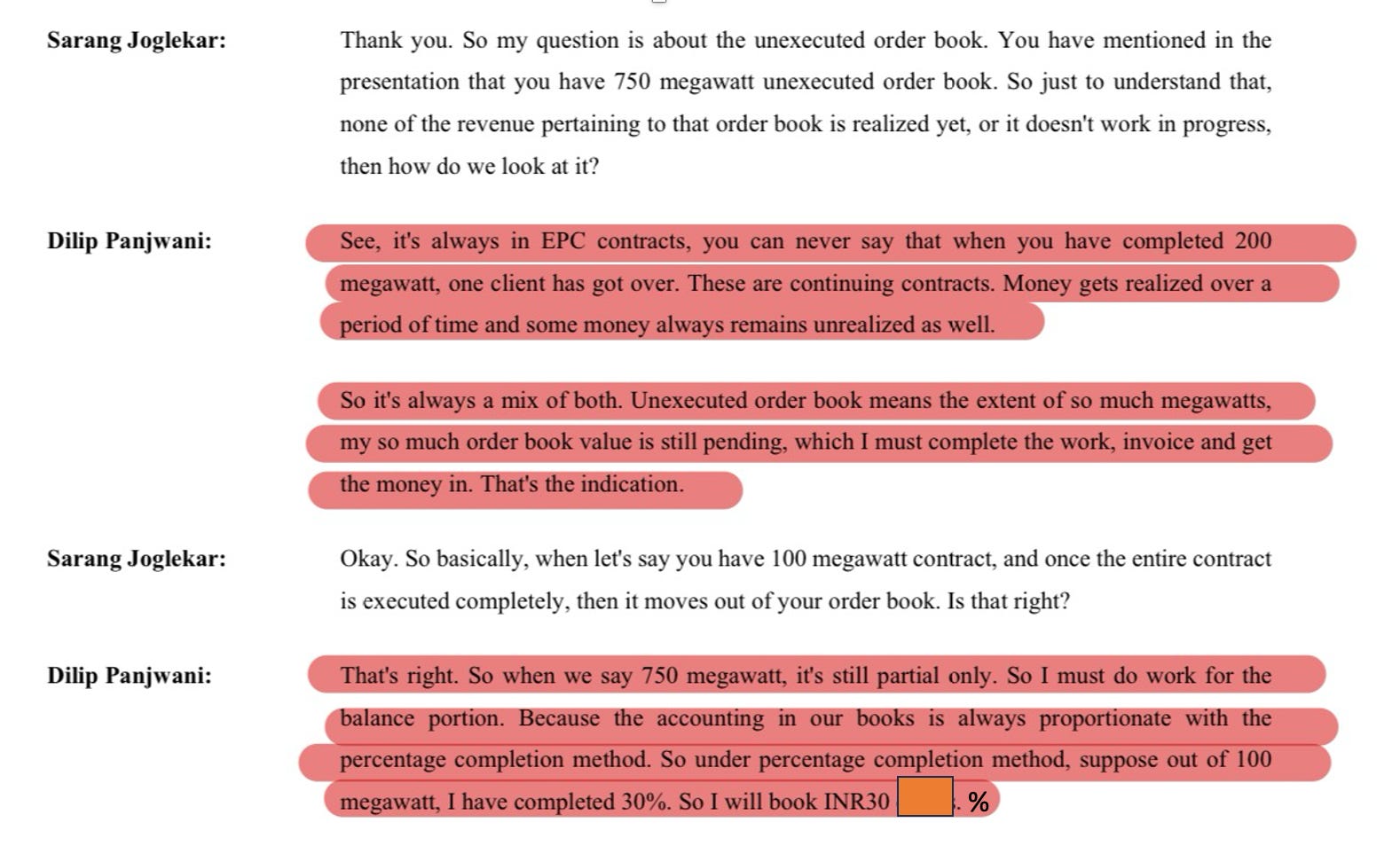

Business by nature is lumpy - because of the different phases of EPC and revenue recognition

There are four phases of the activities in an EPC contract. The first phase is the engineering and the drawing, the second phase is the sourcing of the materials, the third phase is the construction activity and the last is the commissioning of the project.

The engineering and drawing phase of the project is low revenue / low margin component compared to Phase 2 and Phase 3 of the project. Commissioning is the tail end of the project where you realize a bulk of revenue.

Generally in Ql of the year, there are more projects in the engineering & drawing phase and they move into higher margin phases of execution in coming quarters.

O&M Unit economics

Per MW O&M is around 3-4 Lakh and with EBITDA margin of 30-35%. However, normally company gets O&M for smaller projects i.e. sub 200 MW as for bigger projects companies tend to do this in-house.

This is a high-margin annuity kind of business and will keep growing as the company keeps on executing more projects.

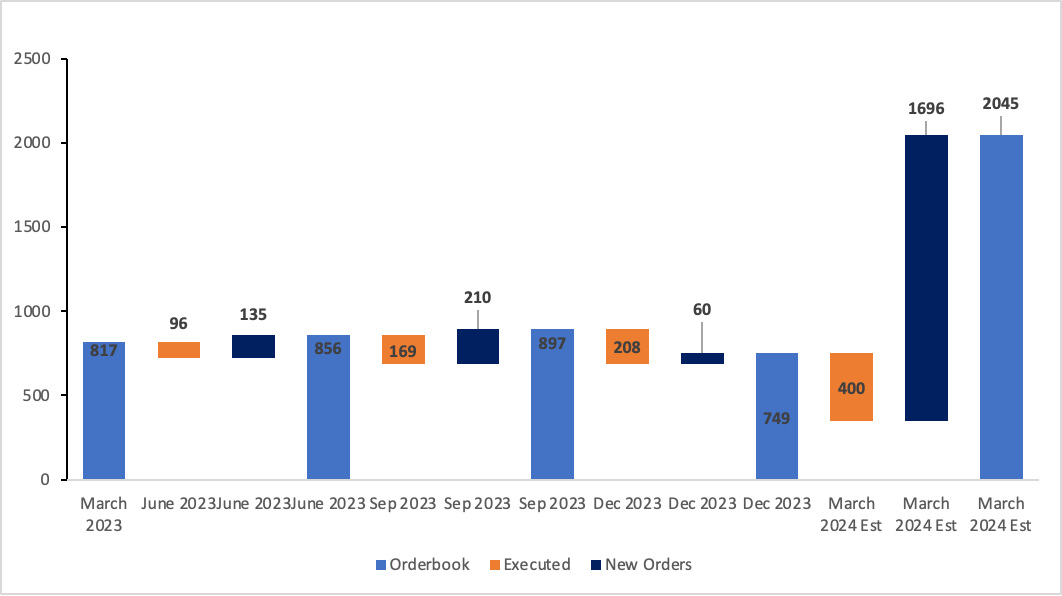

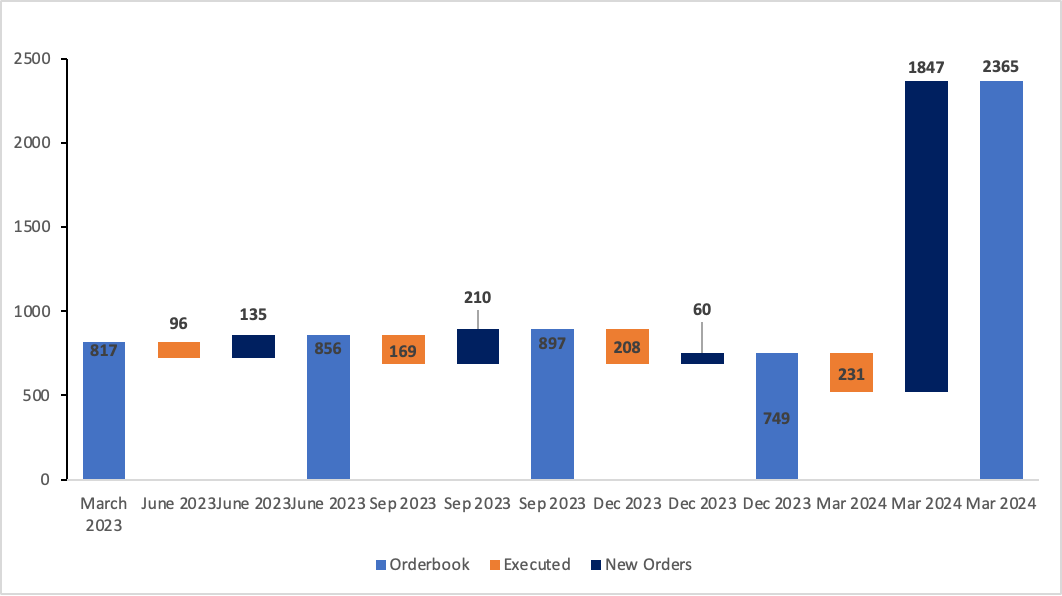

Trend in Execution and Orderbook

Orderbook is expected to become 2.5X from March 2023 to March 2024.

Estimated commissioning of 400 MW as per management comments in the previous concall. New orders based on exchange filings. Has started taking on bigger projects like 980 MW and 412 MW projects which are to be completed in 1 year. The execution of them will be crucial to see.Anti-Thesis Pointers

Shift towards In-house EPC Projects

Execution risk

The core job of an EPC player is to finish the project on time. They need to be very adept in the functions of the business like modules procurement, business development, bidding, project design, finance etc.

If the projects are not completed on time they will lead to cost overrun and will impact the margins severely.

The company is growing at a rapid pace, which needs a substantial pipeline of investable funds. The interest rate fluctuations can lead to shortage of funds to execute projects

Difficulties in procurement / Shortage of raw Materials

ALMM - can be a risk if the sector slows and beneficial as the parent is in manufacturing modules

Corporate Governance / Related parted transactions

There are substantial related party transactions. If they are done at an arm’s length, a minority investor can never be sure of.

They have in the past reported data that is inconsistent. Or if it is on account of change in strategy it has not been clearly communicated.

Even the execution numbers in the initial fillings didn’t match.

Well the company was very small at that point of time. Still make me cautious on the back of my mind.Final Thoughts

The company is in an exceptionally positive industry environment in an asset-light business where they have no capital investments in technologies, infrastructure, or capacities. The determinants of success are bidding responsibly, addressing the project’s scale that they will be able to deliver on schedule along with the highest generation yields, and maintaining financial discipline and balance between margins and growth.

They also have the advantage of being part of a group that has upstream manufacturing capacities and hence capitalize on the captive Group availability of solar modules

Ultimately EPC is a cyclical business - what we have to avoid is peak multiples at peak earnings.

The company can execute 1.75GW in FY2025 (based on 350MW of previous orders to be executed and 1400 MW of orders received in Q4 FY2024 to be executed within 12 months). Assuming all the orders are without modules at 1.25 cr / MW and an EBITDA margin of 15% translates into 325 Crore of EBITDA. Further, as they scale to 3GW of execution (based on 9GW of order pipeline) the EBITDA can be 550 crore plus. The company in the past has scaled fast.

In the end, we can’t be sure where the puck will stop. So we may be at peak margins but can’t say that we are at peak earnings as the growth is visible in India as well as around the globe. At the current Market Cap of ~ 20000 Cr, the valuations sure are stretched. But in high-growth businesses, we can’t be sure how much growth is priced in and for how long the company will grow.

What my strategy will be on the fundamental side is to follow the business closely to see whether they are winning orders, executing orders, walking the talk on margins and not taking too much risk for the sake of growth. Further, I will be executing the investment from a technical viewpoint as there is only so much we can do, and in situations where there is a plethora of possibilities and lots of moving parts, I will depend on the wisdom of the crowd.

Update 11th May 2024

Waaree came with FY2024 results.

Key takeaways from the result:

(1) Commissioned 704 MW in FY24 i.e. only 231 MW commissioned in Q42024 against management guidance of 400-450 MW.

Updated orders bridge

(2) The yearly execution is a record high at 704MW implying 3X FY 2024 required to be executed in 1.5 Years.

(3) Margins at the same level.

What next?

Should one focus on 1 quarter of subdued performance compared to expectations or at large order book in hand?

In my view, the valuations WaareeRTL trades at give no room for error. This quarter signifies that there are scaling issues and execution challenges. However, the business has serious tailwinds and from a long-term perspective should be accumulated at lower levels. *****

Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word! 😀

Thanks for reading. Please do share your feedback.

Connect with me on Twitter: @pankajgarg_ciet

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Disclaimer: I may have a position in the company. My views are biased.

Thought provoking, can be considered for long term investment with low risk high gains.