What shall I call Zomato Ltd.? Is it a consumer company, a technology company, a brand, or a retailer?

To me, it is a confluence of all the above. These characteristics are more like pillars of Zomato’s business. Without technology, the company can’t scale. Without scale the business model is unviable. Riding on changing consumer lifestyles- eating habits and retailing. Branding themselves to have a unique positioning in the market.

ZOMATO Ltd has 3 businesses under its roof:

(1) Food Delivery using Zomato App

(2) Quick Commerce business - Blinkit

(3) B2B Kitchen Supplies - Hyperpure

Business Aspects

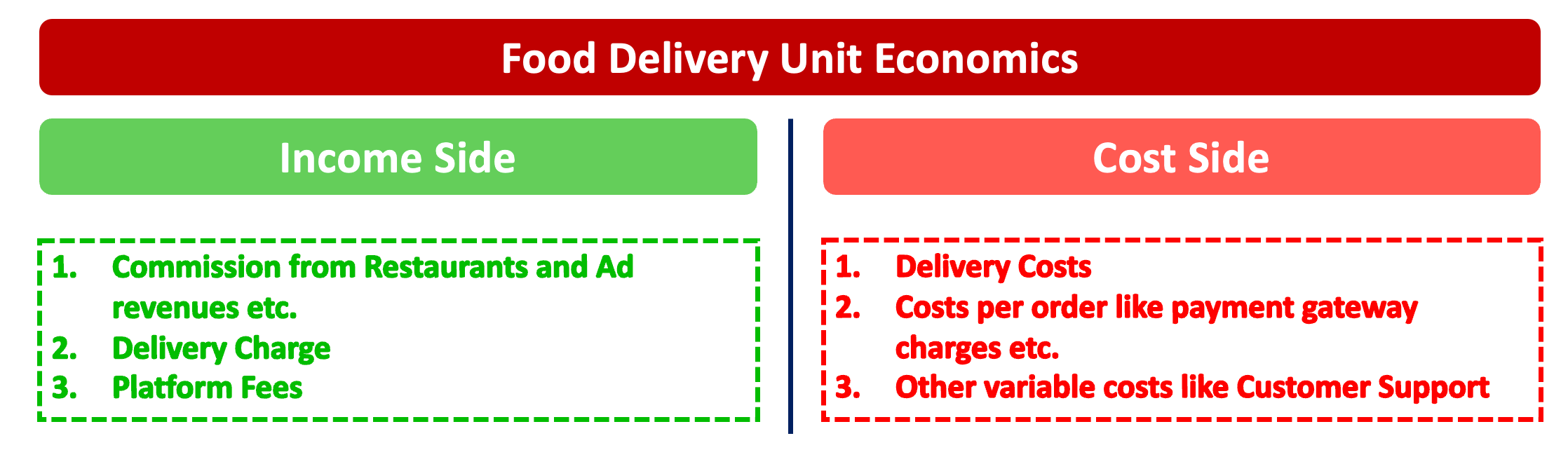

Let’s look at the unit economics…

So if the Income side is greater than the cost side you are on the path to profitability but not yet reached there.

There are other huge fixed costs e.g. technology development, lease expenses, etc. These fixed costs rise in a step function but not to the same extent e.g. if the number of orders scales from 1 lakh to 10 lakh, the fixed costs will not increase 10x…hence decreasing the per-order fixed cost…leading to profitability.

Source: MOSL Wealth Creation Study “Atoms to Bits”

Similarly, the concept holds for Blinkit and Hyperpure as they scale, the per-order costs decrease, spreading the fixed costs over a larger denominator.

Scale up on the back of favorable unit economics (delivery in this case) leads to operating and financial leverage kicking in causing profits and profitability to skyrocket

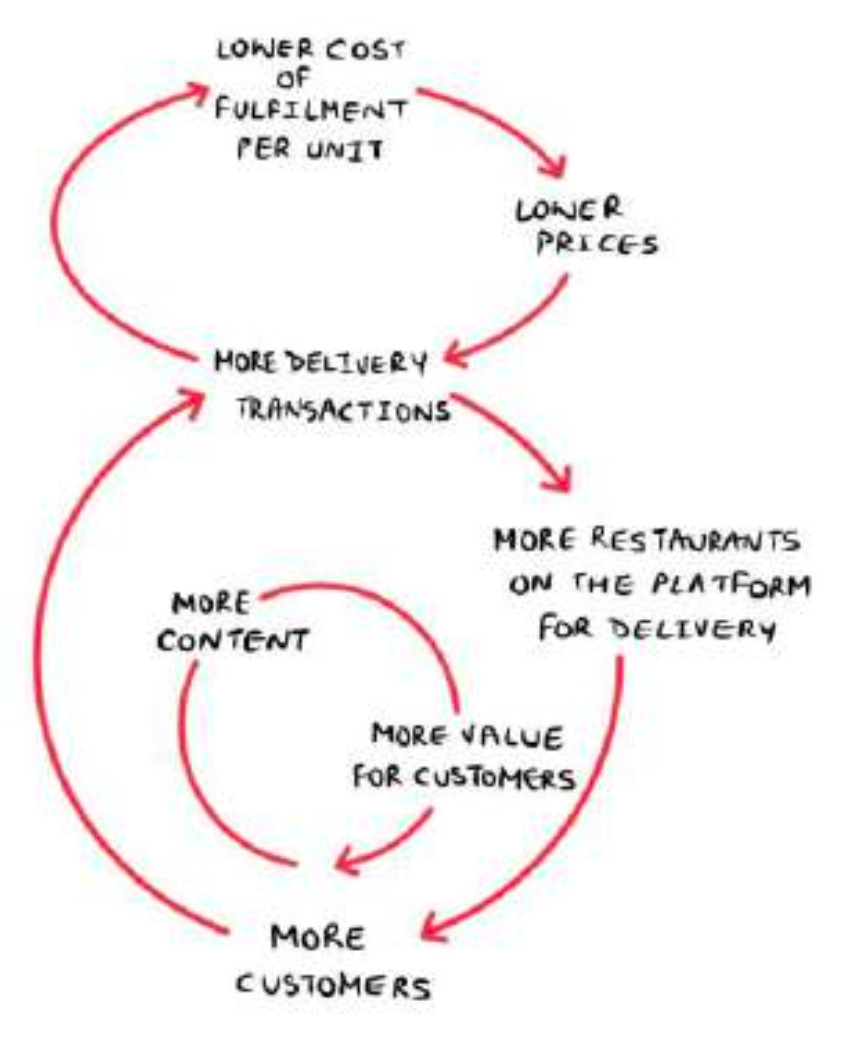

This is a Platform business with network effects…..a virtuous cycle

Source: Zomato DHRP

Zomato benefits from indirect network effects. The greater the number of customers, the greater the value for restaurants and vice versa. So increased choices for customers and a bigger market for restaurants. Plus, the delivery network can be utilized more efficiently.

Zomato also benefits from data network effects as every incremental customer and restaurant adds valuable data. E.g. reviews about a restaurant by customers, understanding consumption habits, etc. It can leverage this data to run marketing campaigns or give personalized recommendations to customers.

Essentially the Hyperpure business leverages relationships with restaurants to source ingredients for them. Even Blinkit leverages data gathered.

This (Blinkit) is not a pan-India model and there is no need for it to be one. This is a hyperlocal model, and the density of the population determines the opening of a store. Zomato has data on population and driving distance. That data is used for Blinkit store mapping.

Essentially the value addition is in helping restaurants and brands get discovered. Enable them to grow their business, serving new customers. Lower cost of starting a restaurant via Zomato and Hyperpure. Enable scaling of D2C brands via Blinkit.

Helps stand-alone/small business owners to compete with larger brands

and is transforming the eating habits

Source: Zomato DHRP

What this table depicts is that… on average the customer spending on their platform increases year on year. The first year may be testing the water like ordering on a special occasion and gradually the customer use case for ordering increases.

In a nutshell Zomato banks on (1) more customers (2) more orders / more order value per customer (3) Increase in restaurant listings

Softer aspects of the business - notes from the book “Culture at Zomato”

Creates lots of jobs - GIG economy

The people we help create livelihoods for-like delivery partners - don’t just work for their livelihoods, they work to provide their kids with access to better opportunities. I have faith that the ecosystem we are building - in just a couple of decades from now - will enable India’s next generation in a massive way

Startup DNA

We don’t run Zomato like a company. We run it like a passion project.

Arrogance is what the beginning of the end looks like. Stay away from hubris and always stay humble because we are always only 1% done.

At no point should you think we are a big company. In fact, big shouldn’t even be an objective. The only objective all of us should have while we build Zomato is to be useful and helpful - to our customers, our restaurant partners, our brand partners, our delivery partners, and our teammates.

Enabling culture

Philosophy of putting the right person who can take ownership, take the right amount of risks, growth mindset, stay on the edge, and become better every day

Risk aversion is one of the biggest reasons for failure. Instead of avoiding risk, think how you will manage downside. Take some risks, and see your way through. There is no reward without risk.

All growth begins with discomfort. Without it, there is no reason to change

We pay a high price to avoid mild embarrassment. Growth lies in discomfort. Embrace those little embarrassments. Asking for forgiveness is better than asking for permission. Never let your fear stop you from doing what matters.

Actively seek contradictions to improve your work. Seek counterpoints from people who think differently than you. Seek experiences that will challenge you. You will better yourself and in the process create better outcomes for the organization.

Blinkit

I’ve not deliberately covered Blinkit here as I have covered in my previous post.

Remember, Blinkit is an even bigger growth engine, with a much larger TAM, and is a value migration play.

"At that time [when it was acquired], it was a culmination of everything that we learned about customer first... Albi Albinder Dhindsa, Founder & CEO of Blinkit, and I had the right amount of trust. Blinkit will be larger than Zomato in one-tenth the time. The scale it brings to the table is huge. We don't really think [about the] portfolio. Blinkit was about wanting something quickly,"

Blinkit Q4 2024 Updates: (Aggressive investment mode on but without cash burn)

It broke even in March 2024.

Storecount at the end of FY2024 is 526. Aim to reach 1000 stores by the end of FY2025. Have a presence in 26 cities but the expansion focus is in the top 8 cities.

Food Delivery Business updates

(1) The Food delivery business has grown 20%+ recently (Q3 & Q4 YoY) even when the demand environment was muted in the restaurant industry. However, QoQ has been muted in Q4FY24.

(2) Ad revenue and platform fees are important levers

In August 2023, it began charging the platform fee of ₹2 per order. In October, hiked to ₹3, in January 2024 it was hiked to ₹4, and again hiked to ₹5 in April.

(3) There is a continuous improvement in the EBITDA Margins in the food delivery business.

Final Thoughts

Has cash balances of over 12000 crore. The good part about cash balance is that it makes the business resilient. However, given the company already has its plate full, there will likely not be an acquisition and this cash will lie idle in the books.

As I alluded to, the company operates with a startup mindset, so they will be experimenting a lot. Shareholders will have to align themselves with the founder. This is an evident brand and business - as a shareholder embrace change and experimentation. Need absolute conviction in the jockey.

Case in point: Zomato has started charging for priority delivery. In my view, this (1) dilutes the Zomato Gold Program and (2) looks like a deliberate attempt for revenue maximization. On the other hand, they have started bunching of orders which is an excellent case of optimizing resources. I would rather like the company to develop algorithms that allow for more of bunching and hence reduce the delivery costs. This can pave way to '“Economies of Scale - shared” as described in the book “Richer, Wiser, Happier”. But ultimately, the shareholders have to believe in the management to execute.

Is the growth in food delivery sustainable? In my opinion there is room to grow.

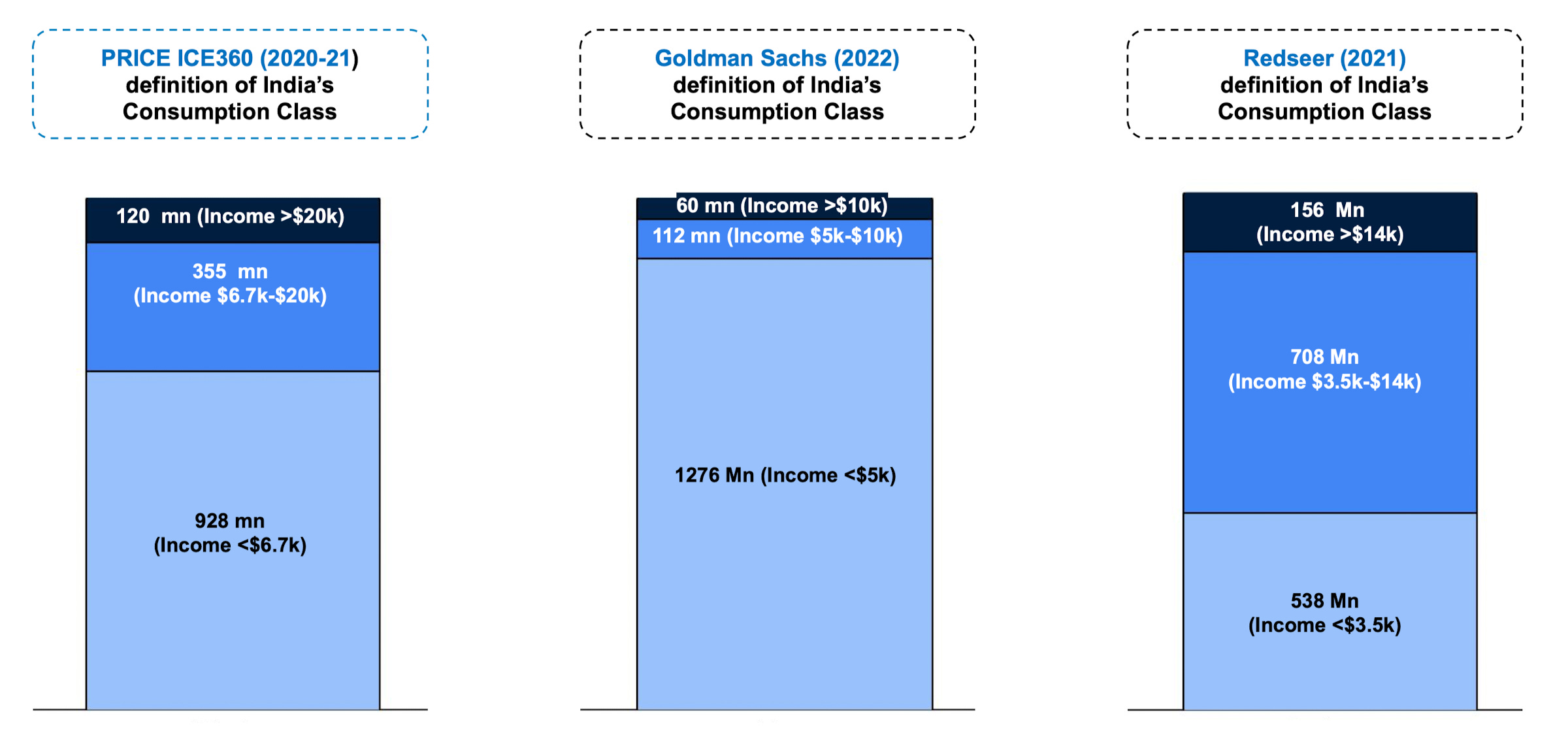

There are 1.9 crore avg monthly transacting customers. Various reports suggest the size of the consuming class in India to be 6 cr to 15.6 cr. Hence the market has room to grow.

Indus Valley Annual Report 2024

On top of this…the consuming class is growing.

Food delivery businesses have essentially become a duopoly. The worst is over in terms of competition for the time being. In investing one can never be sure of competition, customers, innovations, and business models. However, the way things stand today the future of this business looks promising

To Sum Up

The businesses housed in Zomato have room to grow. Currently growing at an exponential rate (over 50% GOV increase YoY).

The business has huge fixed costs and operating costs but on the flip side, it is a scalable business.

Currently in investment mode...but can entail 4%-5% steady state margins. The resilience of the business is being tested where Zomato and Blinkit are growing exponentially in this muted demand environment.

Hockey Stick Growth

Given that the number of stores can in the future bump up to 4000 (500 X 8 top cities) (I am not even looking at the business outside top 8 cities) from the current 526 stores and growth in food delivery and other Zomato's adjacencies we are looking at a hockey stick growth when Blinkit will move from investment phase to profitability path.

At current prices, the stock looks very expensive but let's appreciate the long-term growth embedded in this.

It epitomizes the aspirations of the New India which is tech-savvy, craves convenience and new experiences.

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

In how many centre's/ cities Company operates?

Should be read twice to digest.