Zomato Ltd. - Result Updates: Q1 FY 2025

Zomato Ltd. - Result Updates: Q1 FY 2025

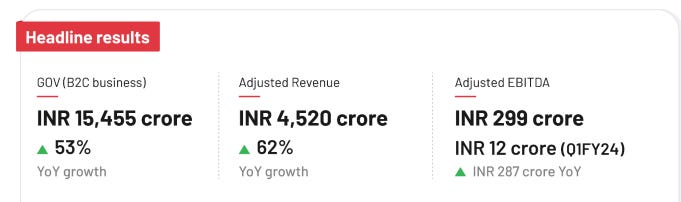

Continued Growth Momentum

Previous posts on Zomato and Blinkit

This 53% growth is the blended growth in Food Delivery, Blinkit, and Going out business

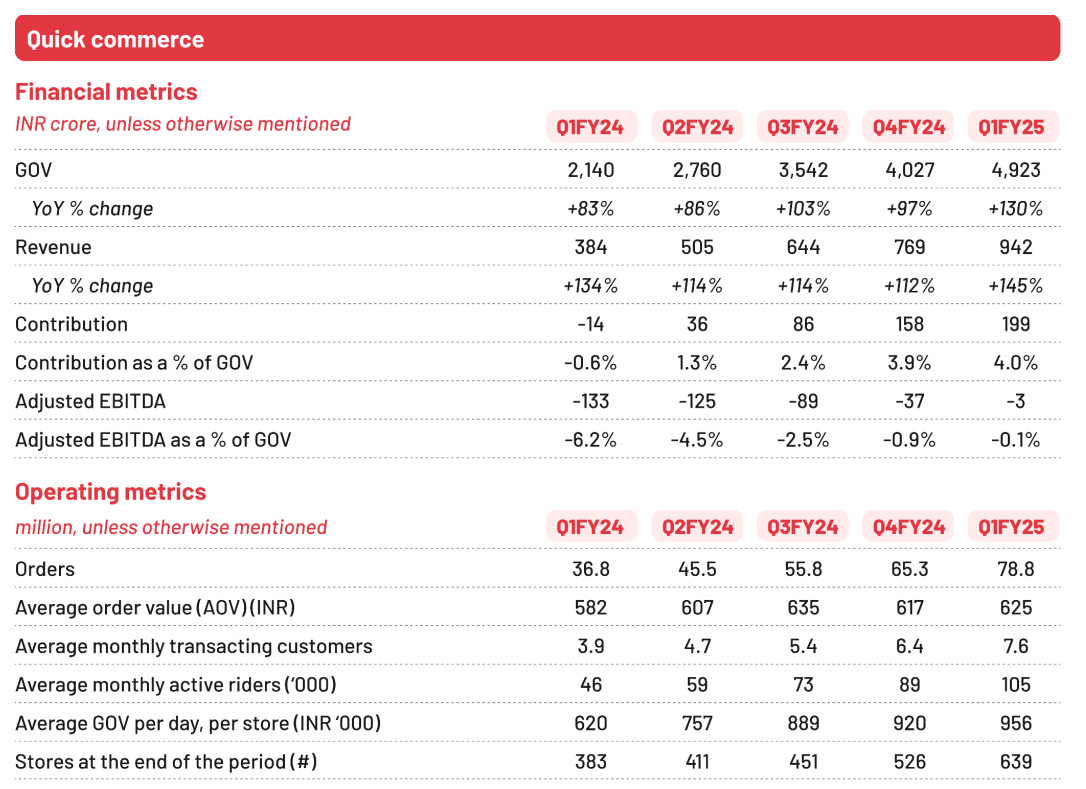

Quick Commerce Business

Added 113 stores (Blinkit)

Targeting 2,000 stores for Blinkit (mostly concentrated in the top 10 cities). Current store count is 639.

3X in 3 years 😲Beyond the large cities, the size of the market is still undiscovered

GOV for top 50 stores is INR 18 lacs per day per store, and growing.

This shows the potential of business model and the fact that GOVs will be on upside trajectory.

It will be very wrong to assume humungous growth in all stores as pareto principle kicks in whereby few stores will contribute dispproportionately to revenue (you need other stores as well for network effects and logistics)

Overall the GOVs are expected to expand.Average selection available to customers in any neighborhood has increased between 4-5x over the last eight quarters - now offering up to 25,000 unique SKUs in some locations.

This in my opinion is the most challenging task for the competitors to crack. How far they can expand offerings without diminishing returns has to be seen.

Handling number of SKUs is the differentiating factor between different retail models like Kirana, Convenience Store, Super Market, Hyper Market and E-Commerce. Competitive intensity in the quick commerce category has been high since the word ‘quick commerce’ was coined. Recently, some players have been spending more on marketing and subsidies. However, our customers, who value quality of service and reliability, seem to be unaffected and that reflects in our performance of the quarter, where we have grown 20%+ without the need to match the spends or subsidies of our competitors.

I don't agree completely with this statement.

Lets invert this statement...If they are not taking away share from others that means they are generating new demand which did not exist before i.e. Impulse purchases which the customer would not have otherwise.

If all the purchases are impulse driven or luxury / wealth effect driven then when the tide will turn in economy...Blinkit will be hit the worst.

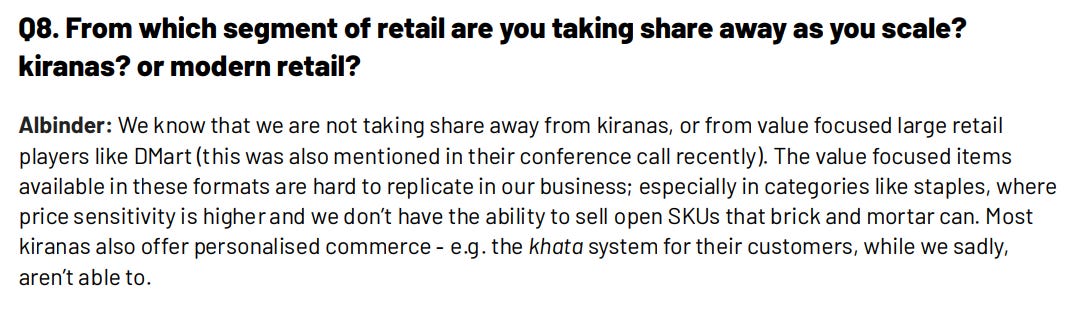

I believe there is some new demand creation by Quick Commerce Companies plus they are definitely taking away share from kiranas and e-Commerce.

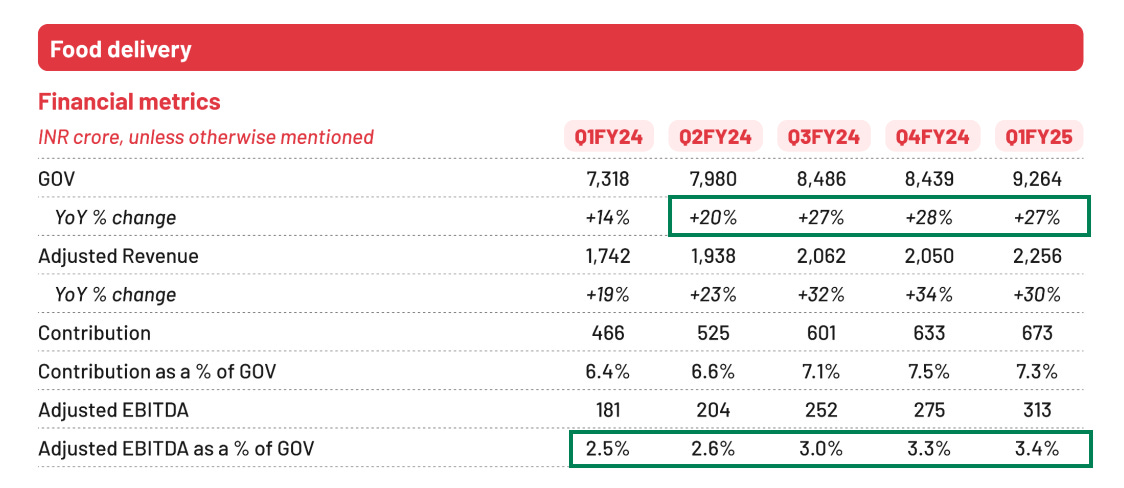

Food Delivery Business

Remain on track to get to 4-5% Adjusted EBITDA margin (currently at 3.4% in Q1FY25)

Once we achieve that goal, our mindset is to maintain margins at those levels and invest any incremental gains into more aggressively improving the long-term health of the platform.

Going Out Business

Expand our going-out offering, building on top of our dining-out business. Additional use cases for customers in the going out space include - movies, sports ticketing, live performances, shopping, staycations etc., some of which we have already launched, or are building as we speak. Building a one stop destination app for going-out could be a game changer for each of these use cases, and we intend to do exactly that with our new District (by Zomato) app. If we execute this well, we see going-out becoming the 3rd large B2C business emerging out of Zomato.

New App for going out business.

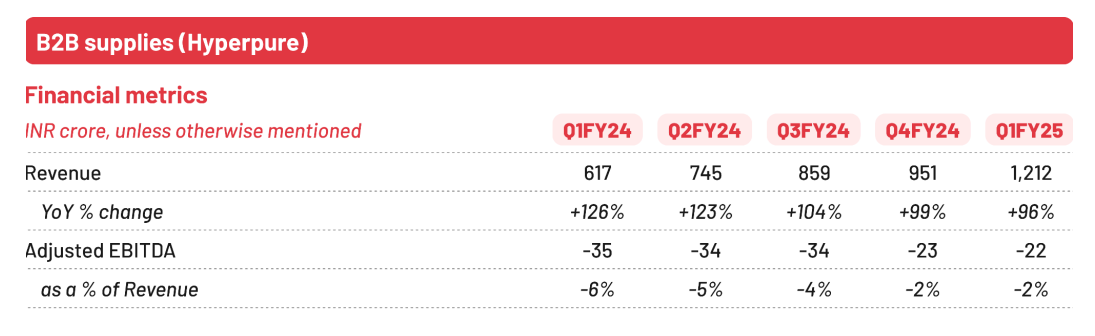

Another avenue benifiting from rise in disposable income / growth in consumer dicretionary space.Hyperpure

This segment has not been paid attention to in the letter to shareholders but this is the second largest segment after food delivery.

My viewpoint

(1) Valautions give no room for error

(2) Quality of the growth (especially Blinkit as this is the main future driver)

If we have to make long term investment thesis than I am not just interested in the headline growth...but the quality of growth itself. What I mean is that I don't want mindless addition to stores, the addition should have tangible benefits of strengthening the network as well as adding profitability in due course.

In this Quarter the company has managed to add stores without making loss i.e. whatever net profit they were making from matured/profitable stores gets equated with loss from new stores. Essentially because of operating leverage the operating cost of incremental store reduces.

Will the same be the case in rest of the store additions till 2026? I don't know but trust the management to take right decisions. Ideally the EBITDA of Blinkit should not slip back in Red.

(3) Broadly the results are in line with the expectations of high growth Market’s reaction to results

Gap up and sustaining. Thumbs up by the market

Resources: Letter to Shareholders

*****

Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

Free course by Vivek Mashrani

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Thanks for reading Pankaj’s Substack! Subscribe for free to receive new posts and support my work.