Result Updates: Zen Technologies Q1 FY2025

Result Updates: Zen Technologies Q1 FY2025

Solid Growth and Solid Future Guidance

Check out the detailed note:

Key takeaways from Q1 / FY2025 results:

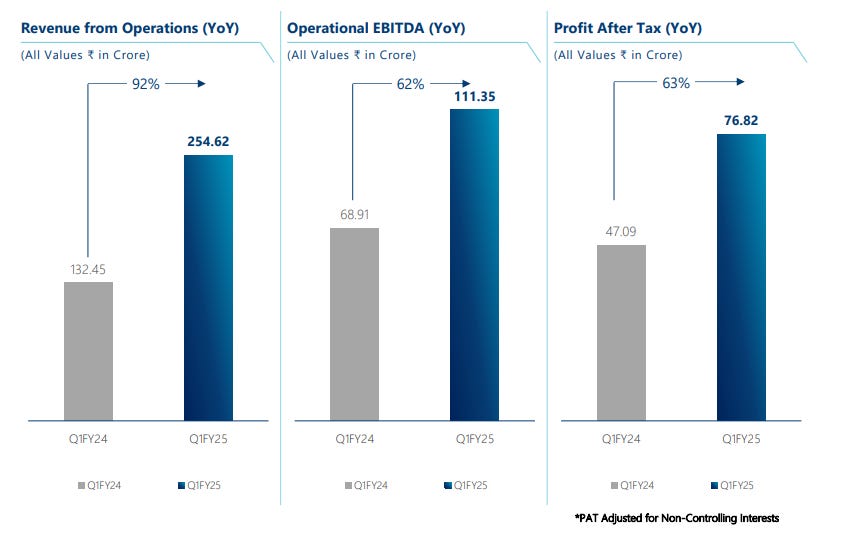

(1) Strong Execution - Blockbuster results. 92% revenue growth, 62% EBITDA growth and 63% PAT Growth (YoY)

(2) Strong Guidance - Infact Guidance Intact that they will do 900 cr revenue in FY2025 with ~35% EBITDA Margin and ~25% PAT margin

Our strong balance sheet and ongoing investment in R&D ensure we remain at the cutting edge of technology, ready to meet evolving customer needs. We are excited about the future and confident in meeting our guidance of ₹900 crores of turnover in the current financial year. - Press Release

(3) Business to be looked at on a full-year basis. Don’t focus on Quarterly gyrations. Product mix may change and execution could be lumpy. Have healthy enquiries for both their businesses i.e. Simulators and Anti Drone

(4) Zen had recently unveiled 4 new products. The exact demand for these products is not yet researched. They are AI-enabled products that will serve as an extension to the forces or the anti-drone systems.

Market size for these products is in 1000s of crores however detailed study is required to know the market size. There will be more announcements in this area.

(5) New Orders will come predominately in Q4.

(6) Simulators

15000 cr is the opportunity size

High margin segment with ~40% EBITDA

What drives this segment?? - Huge cost savings, and reduced downtime. etc.

Simulator induction is at a nascent stage + new platforms will require simulators

Why AMC matters and why simulators are not done by OEMs themselves

(7) Anti-drone Systems (ADS)

Demand to be revised upwards from 10,000 cr

EBITDA margin in this segment ~30%

ADS are now in the IDDM list. The only other player is BEL.

Here I have two thoughts

Positive

(1) BEL does many other things so ADS will be one segment of what they do. However, for Zen, this is a focus area. So the development and edge Zen can have in this space are higher.

Negative

(2) BEL as a PSU will get that benefits

(3) Given this space is a new area of activity in modern warfare, new companies will crop up in this space...sooner or later(8) QIP

Enabling resolution - not raised funds yet

Looking for inorganic opportunities as well

(9) 50% CAGR is this sustainable?

Well, management is confident. They expect more and more orders, especially from the Indian Army. They are targeting import substitution and this is what the government's priority is.

Anecdote from concall

The leading indicator of growth is the order book. So fundamentally if the orderbook falters, it is the time to bail out as stocks are being priced to perfection.Market reaction post results

Market so far has reacted positively. Zen moved to ATH territory before the results.

After the results, it made two upper circuits on increased volumes. Has held up the gains.

Strong TechnicallyMy take

The M.cap is still 15000 cr. They are rapidly growing and things like growth in simulators and ADS makes sense if you look at the customer perspective.

Simulators you need to train - it is an effective way to train and given the nature of modern-day warfare ADS are crucial components.

Key Monitorable from Concall: Order wins by Q4, execution in between, and new products

*****

Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

Free course by Vivek Mashrani

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Thanks for reading Pankaj’s Substack! Subscribe for free to receive new posts and support my work.