Personal Finance is Personal

Personal Finance is Personal

Find what works for you...

Wealth is what you don’t see - Morgan Housel, author “The Psychology of Money”

Personal finance is an umbrella term for financial decisions. How much to save? What are our financial goals? Where to invest? How to plan for retirement?

Your goals, behavior, and attitude to money are unique, as are your circumstances and risk profile. So if you come across generalized gyan, especially from finfluencers who behave like know-it-alls…be very wary.

No disrespect…but this kind of advice is a disaster when generalized.

Personal finance is planning for the financial aspects of your goals & desires. It is not a one-way street but a feedback loop, an introspective journey to understand what we value most in life.

To bring your dreams and desires to fulfillment, you must be successful with money.

I am not a certified financial planner and not here to give portfolio advice….I am sharing my learnings in this field and viewpoints on how to go about DIY Financial planning

(1) Learnings from The Richest Man in Babylon

If I have to summarize the core wealth-building principles from this Financial Independence Bible are: work hard, save money, make money work for you, learn from mistakes, and become wealthy.You cannot arrive at the fullest measure of success until you crush the spirit of procrastination within you.

Work attracts friends who admire your industriousness. Work attracts money and opportunity. “Hard work is the best friend I’ve ever had.”

Stick with the plan. Money accrues surprisingly quickly and debts are gone fast with discipline and consistency.

Money is plentiful for those who understand the simple laws of making money. The 7 simple rules of money:

1) Start thy purse to fattening: Save money. You should save at least 1/10th of what you earn. More if you can afford to do so.

2) Control thy expenditures: Don’t spend more than you need. Don’t spend your money as soon as you earn it. Do not confuse your necessary expenses with your desires.

3) Make thy gold multiply: Invest!! (However, asset allocation is personal)

Put your money to work by making smart investments and taking advantage of time and compounding interest.4) Guard thy treasures from loss: Avoid investments that sound too good.

Don't get lured by quick rich schemes. You will be helping the person on the other side get rich quick at your expense.5) Make of thy dwelling a profitable investment: Own your home.

Crunch the numbers to see what makes sense for you at this particular point in your life - Rent or Buy??

In the modern context, home ownership is personal. My personal opinion is to sort out other goals before you commit for house. 6) Ensure a future income: Protect your family with life insurance. Ensure a future income. Every person gets old. Make sure your income will continue without work.

7) Improve thy ability to earn: Strive to become wiser and more knowledgeable. Increase your ability to earn. Improve your skills. As you perfect your craft, your ability to earn more increases. The more we know, the more we may earn. The person who seeks to learn more of their craft becomes capable of earning more.

(2) Learnings from Robert Kiyosaki

Money does not make you rich. Your Financial IQ does.

Case in Point:

Give 1 cr to a person with a low financial IQ and a person with a high financial IQ. Over time you’ll see the difference in how that money is spent and grown.

This is the reason why lottery winners go bankrupt.

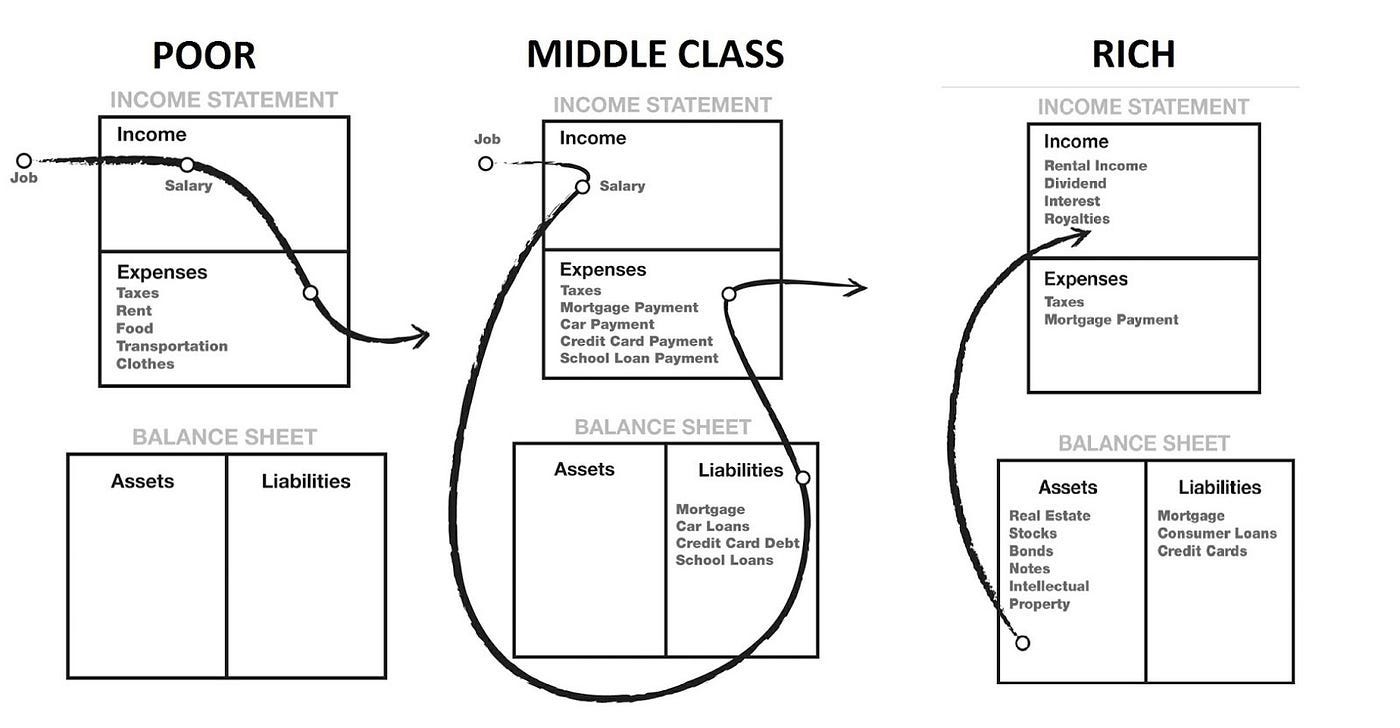

Financial IQ can be acquired with learning about finance....this is not an innate skill Have you wondered what your Personal Financial Statements look like:

(1) Your Income Statement

(2) Your Balance SheetHere is an infographic from Rich Dad, Poor Dad

Do you know how much you earn and spend in a year? How and where your money goes? This exercise is, imo a starting point to understand your relationship with money.

Cashflow Quadrant

The CASHFLOW Quadrant represents the different methods by which income or money is generated … Different methods of income generation require different technical skills, different educational paths, and different types of people.” - Robert Kiyosaki, Cashflow Quadrant

It is not necessary to categorize only in one quadrant. e.g. I have a job and I am in investing, I categorize myself to be in Quardant E and I. (3) Behavior > Intelligence

Our behavior and habits have a long impact on wealth accumulation. Recognize your limitations. We mortal beings are emotional ones. Our actions can’t always be rational but fraught with fear, greed, overconfidence, anchoring bias, loss aversion, familiarity bias, and many more ways biases creep into our decision-making.

Stick to a process. Keep Evaluating. Keep Iterating.

Do what you can easily follow don’t over-optimise. Personal Finance is Personal

***Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

Free course by Vivek Mashrani

Supporting my work

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word!

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not a buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Thanks for reading Pankaj’s Substack! Subscribe for free to receive new posts and support my work.