Energy Transition #3: Transmission Challenge and Opportunity

Energy Transition #3: Transmission Challenge and Opportunity

Part 3 of the Energy Transition series

Recap: To tackle climate change (1) The world has to be more and more electrified using renewables (2) Where electrification can’t fit the bill, we need alternative strategies like Green Hydrogen, etc. to decarbonize

If you haven’t read it yet, I would recommend to go through this post:

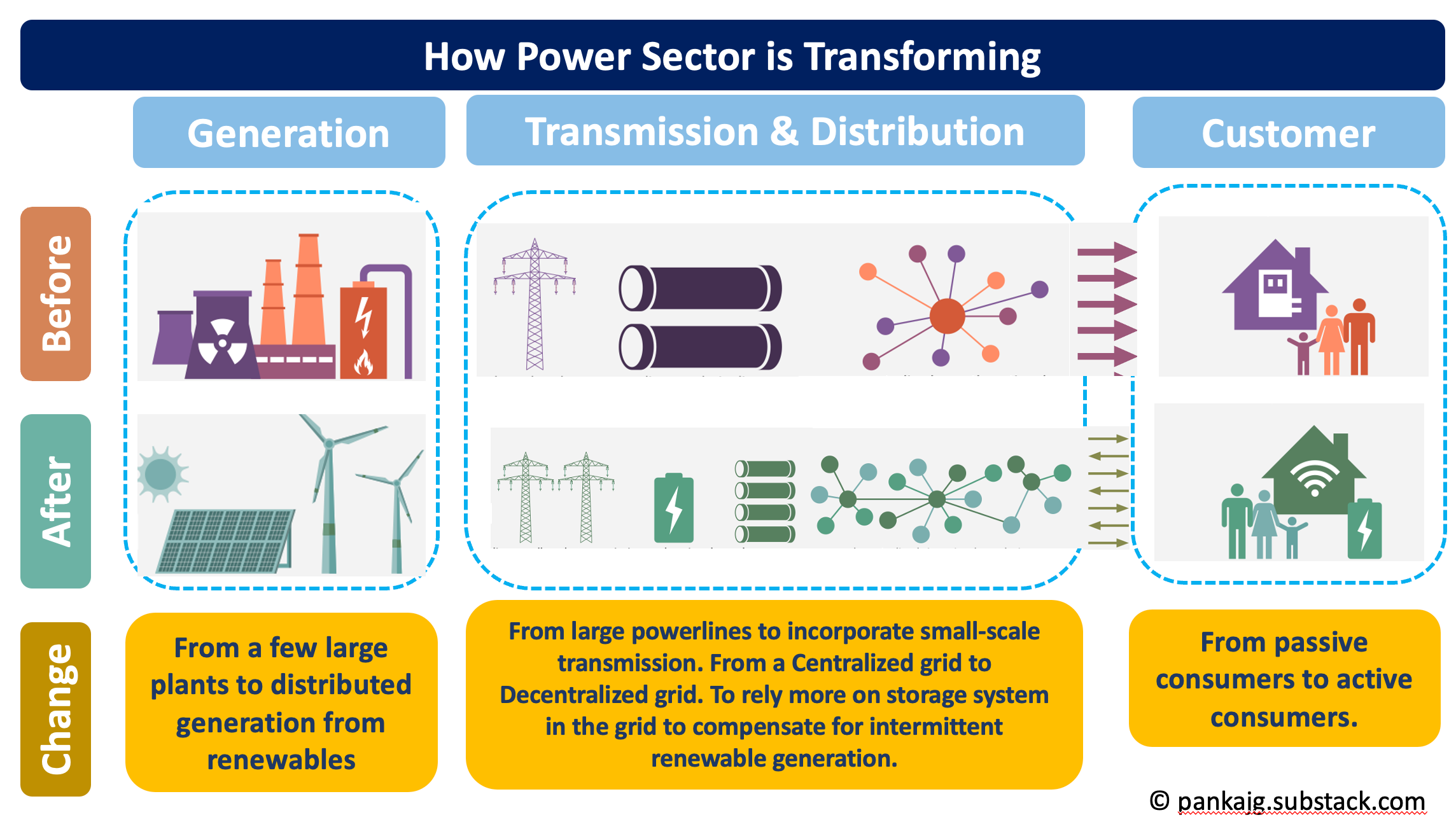

One of the important pieces of the energy transition puzzle is transmission. In the past transmission was simpler, but now transmission itself is evolving as the power generation gets decentralized with renewables. There is a humongous task to be carried out in transmission space for a cleaner future.

Power Sector is undergoing a fundamental shift

On the supply side, (1) our electricity needs are going to be accelerated as we electrify (2) This incremental demand will mostly be catered via renewables predominantly, Solar PV and Wind (Offshore and Onshore). Hence we are looking at more distributed sources of generation.

At the consumption end, the Consumer’s role in the new power ecosystem is changing from a passive (i.e. consume and pay) to an active one. e.g. the consumer is not only consuming, but generating as well (eg. roof-top solar; net metering, captive renewables by Industries, etc.) and the consumption can very well be analytics-driven, for example, economic models may come up that help match the peak supply with peak demand.

What does this change mean for the middle part of the Power Value Chain i.e. Transmission & Distribution?

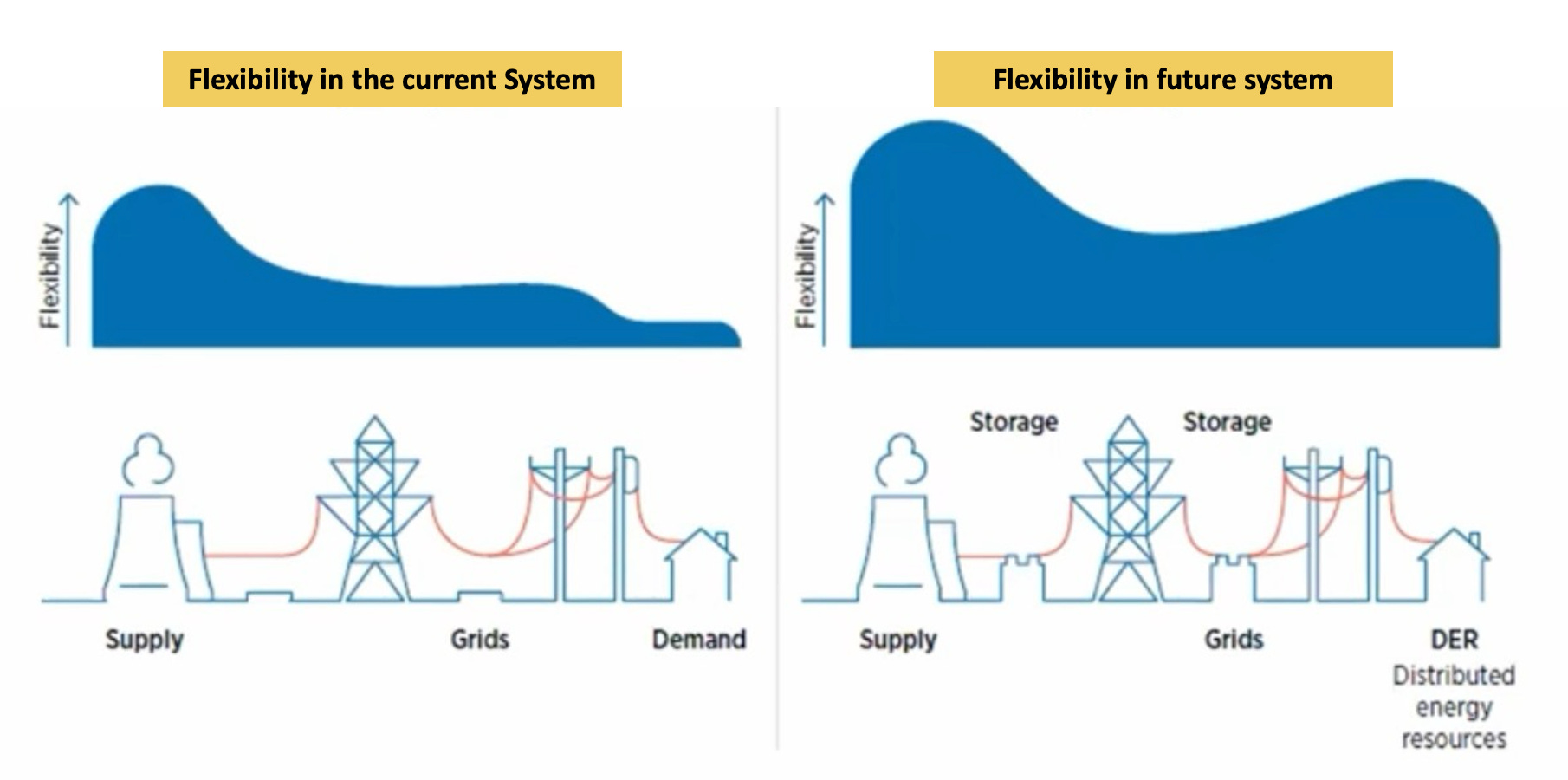

In the conventional power ecosystem, demand is the driving force. The grid infrastructure is designed for peak demand. Also, we can run the Power plants at a lower capacity when demand is less. It is common for coal plants to run at a 60% Plant Load Factor.

When renewables take the forefront in Power Generation, power supply is the driving force. There is no incentive to stop production from solar/wind as the incremental cost of production is minuscule.

So we need to add buffers to store extra power through storage and try to match peak demand with peak power.

Grid Infrastructure: The Bottleneck in the Power Sector

What does the Electrification push mean for Grid Infrastructure? Here are some excerpts from IEA:

Quantum of work:

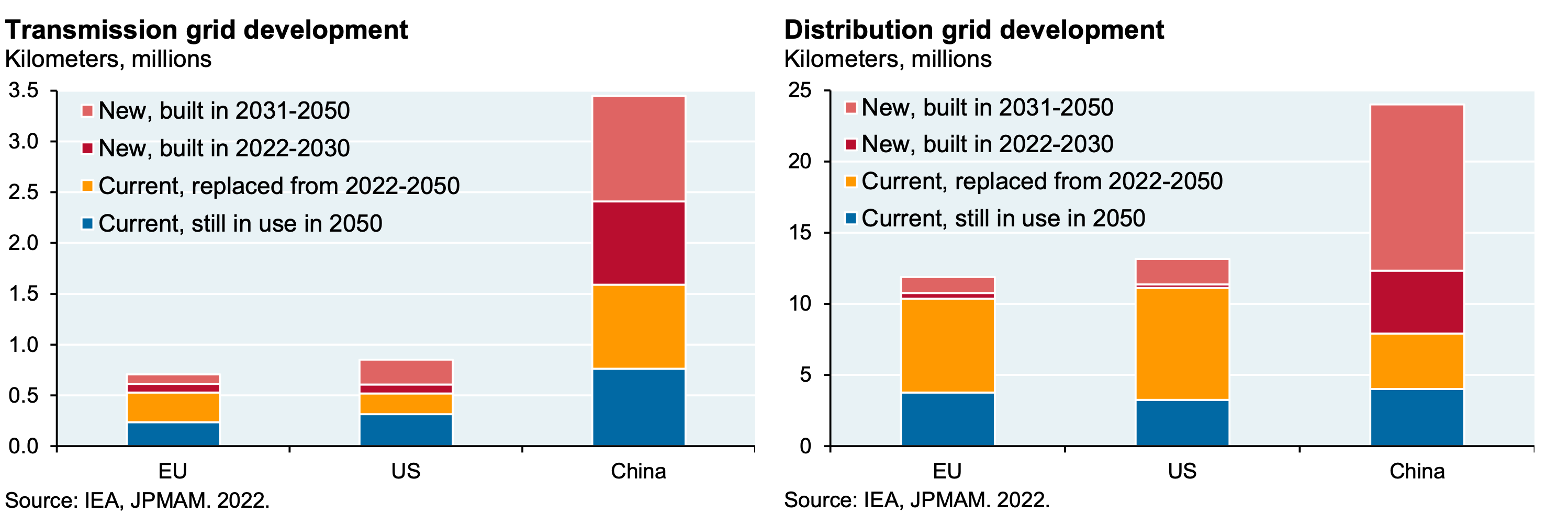

“Reaching national goals also means adding or refurbishing a total of over 80 million kilometers of grids by 2040, the equivalent of the entire existing global grid.”

Urgency:

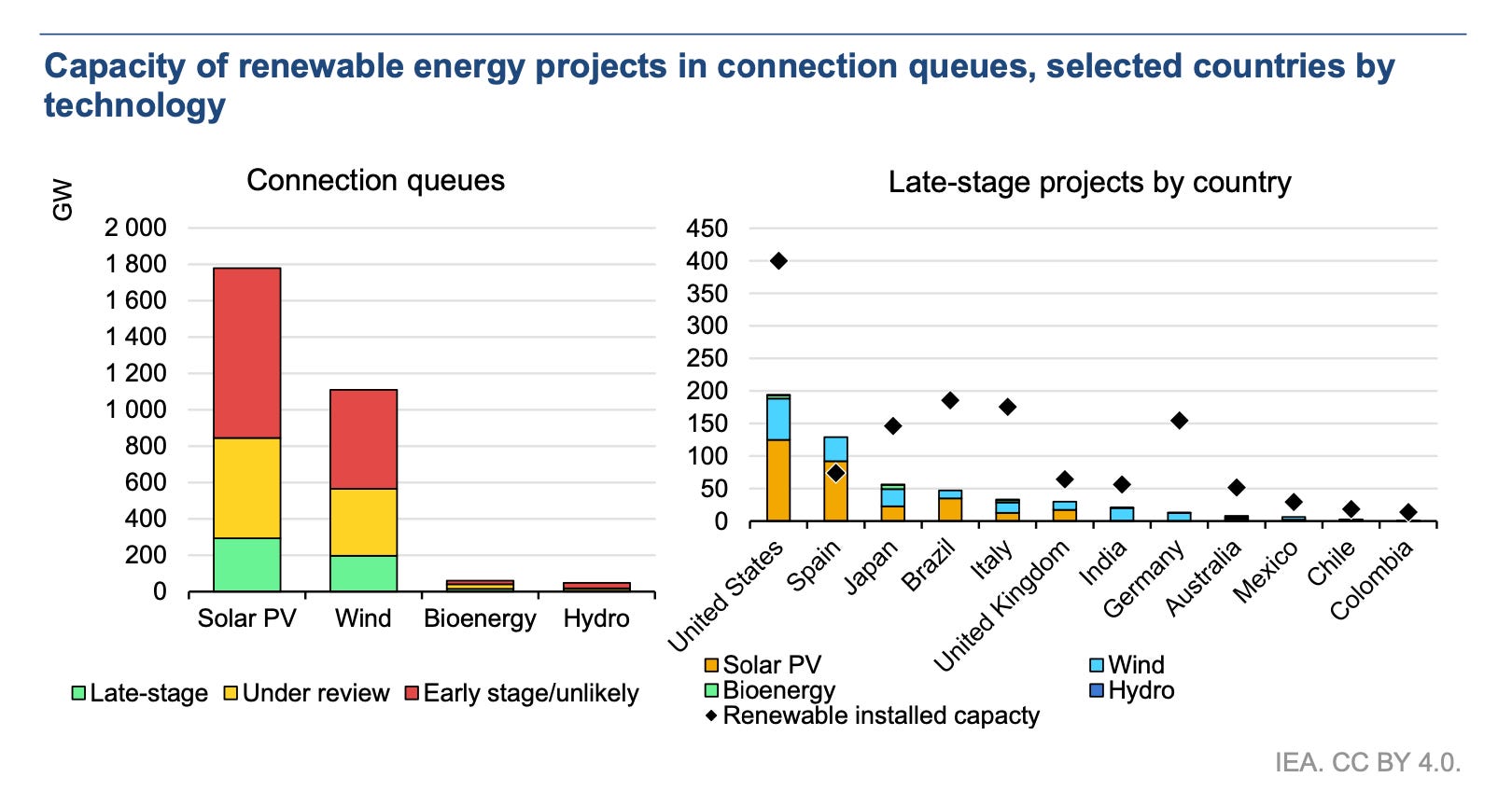

At least 3,000 gigawatts (GW) of renewable power projects, of which 1,500 GW are in advanced stages, are waiting in grid connection queues – equivalent to five times the amount of solar PV and wind capacity added in 2022.

Current Status:

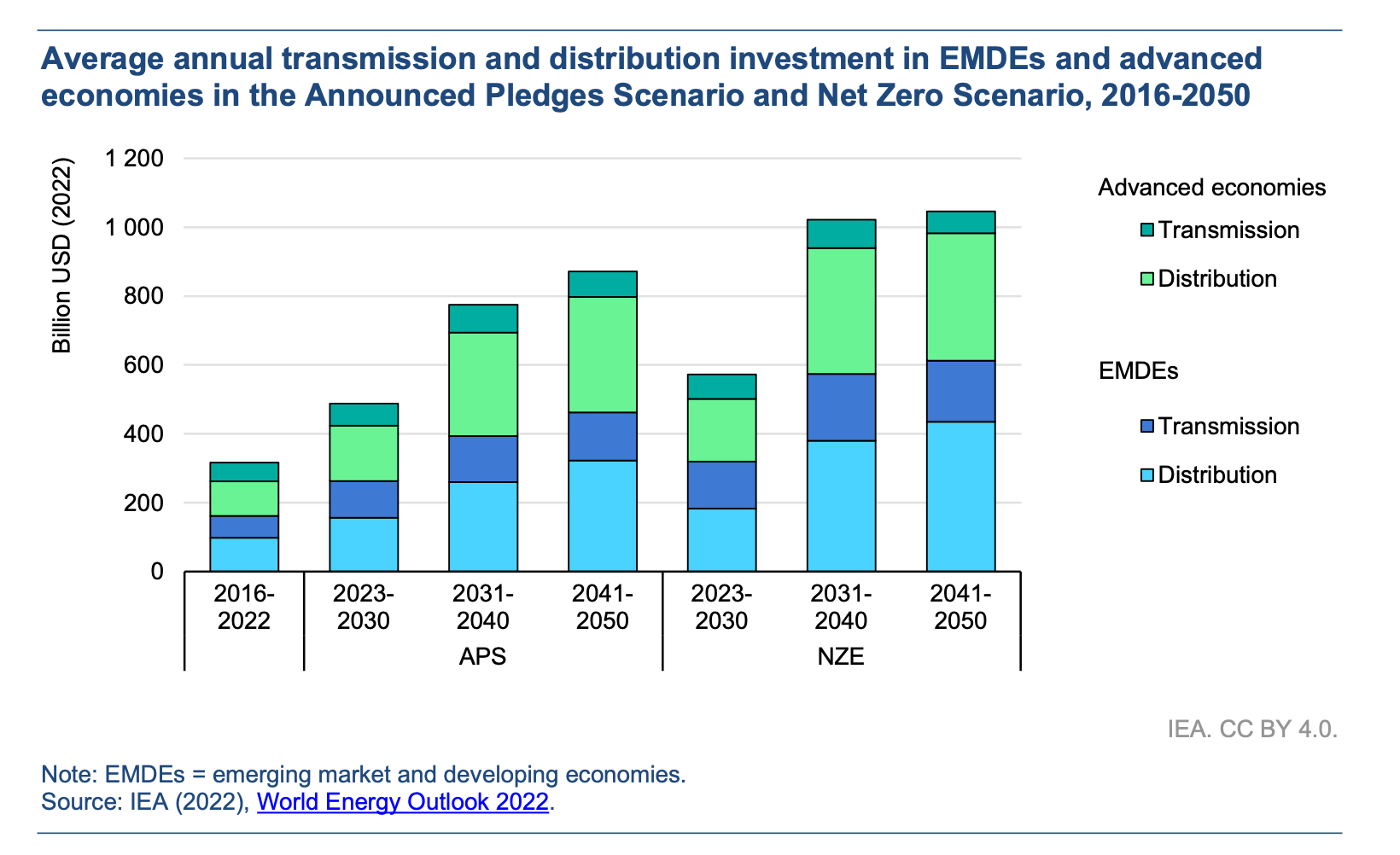

While investment in renewables has been increasing rapidly – nearly doubling since 2010 – global investment in grids has barely changed, remaining static at around USD 300 billion per year. A significant jump (2X-3X) in T&D investments is required

In nutshell, we need to add a lot of Grid Infrastructure, that too urgently while the issue is not being addressed promptlyIdeally, Grid Infra should be built proactively

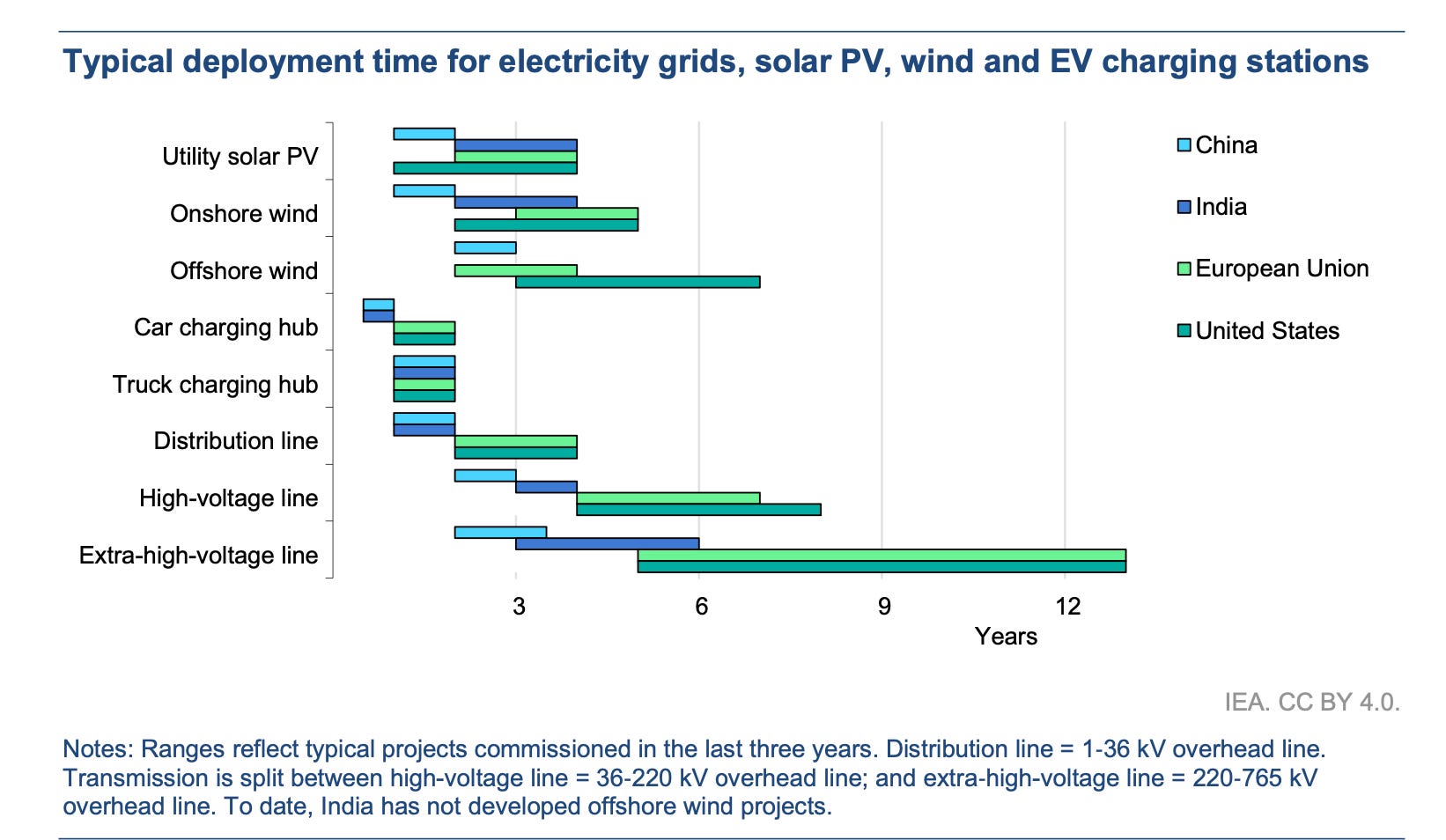

It takes much longer to plan and create grid infrastructure than to commission renewable capacities and charging infra. If the grid is not ready before the commissioning of new capacities, the power assets lay idle.

eg. grid infrastructure requires 5 to 15 years to deploy, while renewable projects take 1-5 years and new EV charging infrastructure less than 2 years to deploy.

Emerging Trends

The following trends are emerging:

1. Need for Smart Grids

Smart Grid: An intelligent electrical network with a two-way flow of energy and real-time information between power generation, grid operators, and consumers.

The Grid of the future has to have real-time flexibility, rapid response, and dynamic load balancing, and be Digitized. Essentially we need Smart Grids.

One way vertically integrated grids will give way to node-based distributed networks2. Interconnect Grids

Interconnection of grids leads to improved grid stability, increased energy security, and enhanced flexibility in managing power demand and supply fluctuations. It also enables access or renewable power in regions with higher demand or less generation capacity. Further, economic benefits can be derived through power trading.

Side Note: OSOWOG Initiative

The initiative aims at connecting energy supply across borders. The vision behind the OSOWOG initiative is the mantra that “the sun never sets”. The OSOWOG initiative aims to connect different regional grids through a common grid that will be used to transfer renewable energy power and, thus, realize the potential of renewable energy sources, especially solar energy.

Read more at the International Solar Alliance (ISA) Website

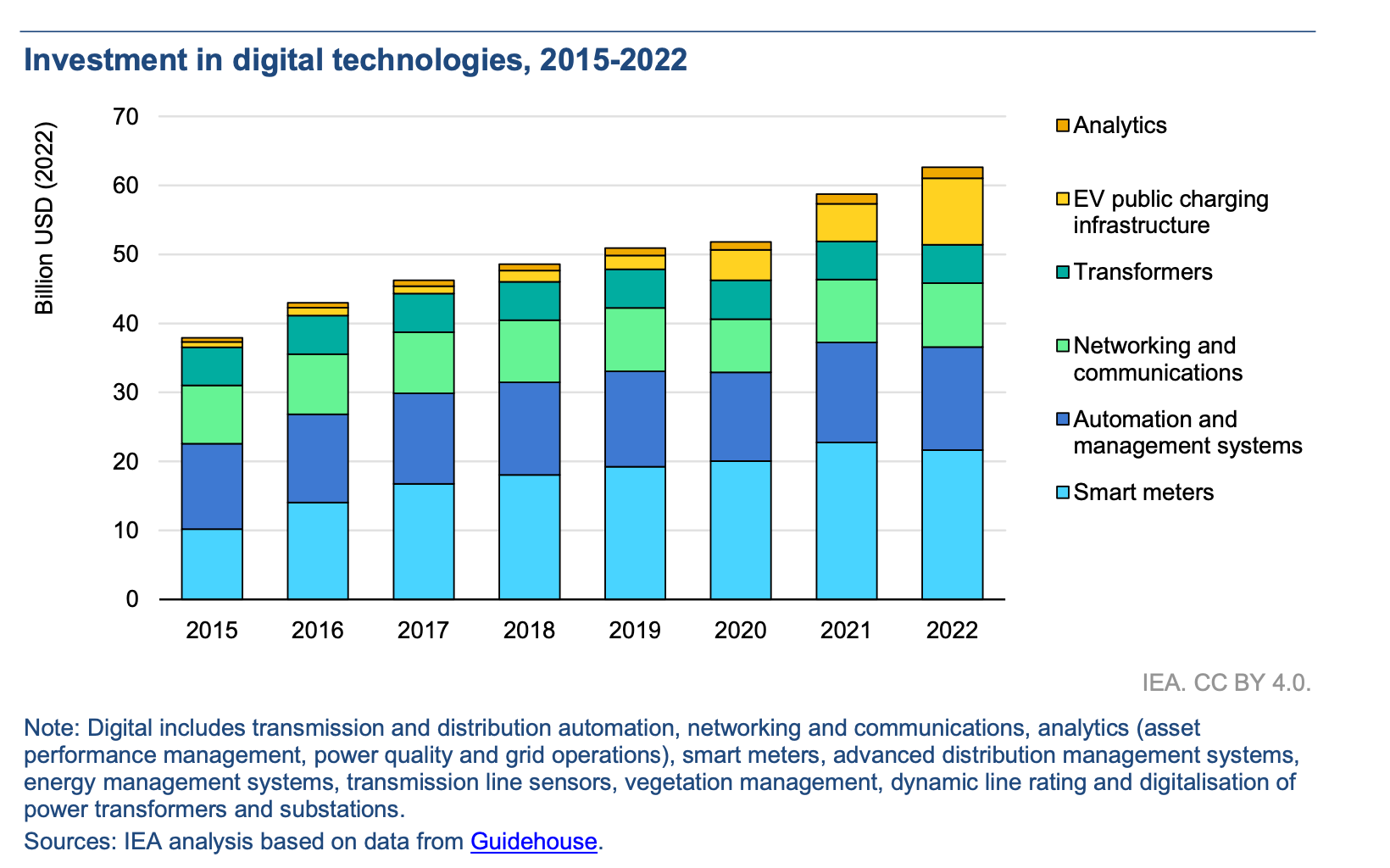

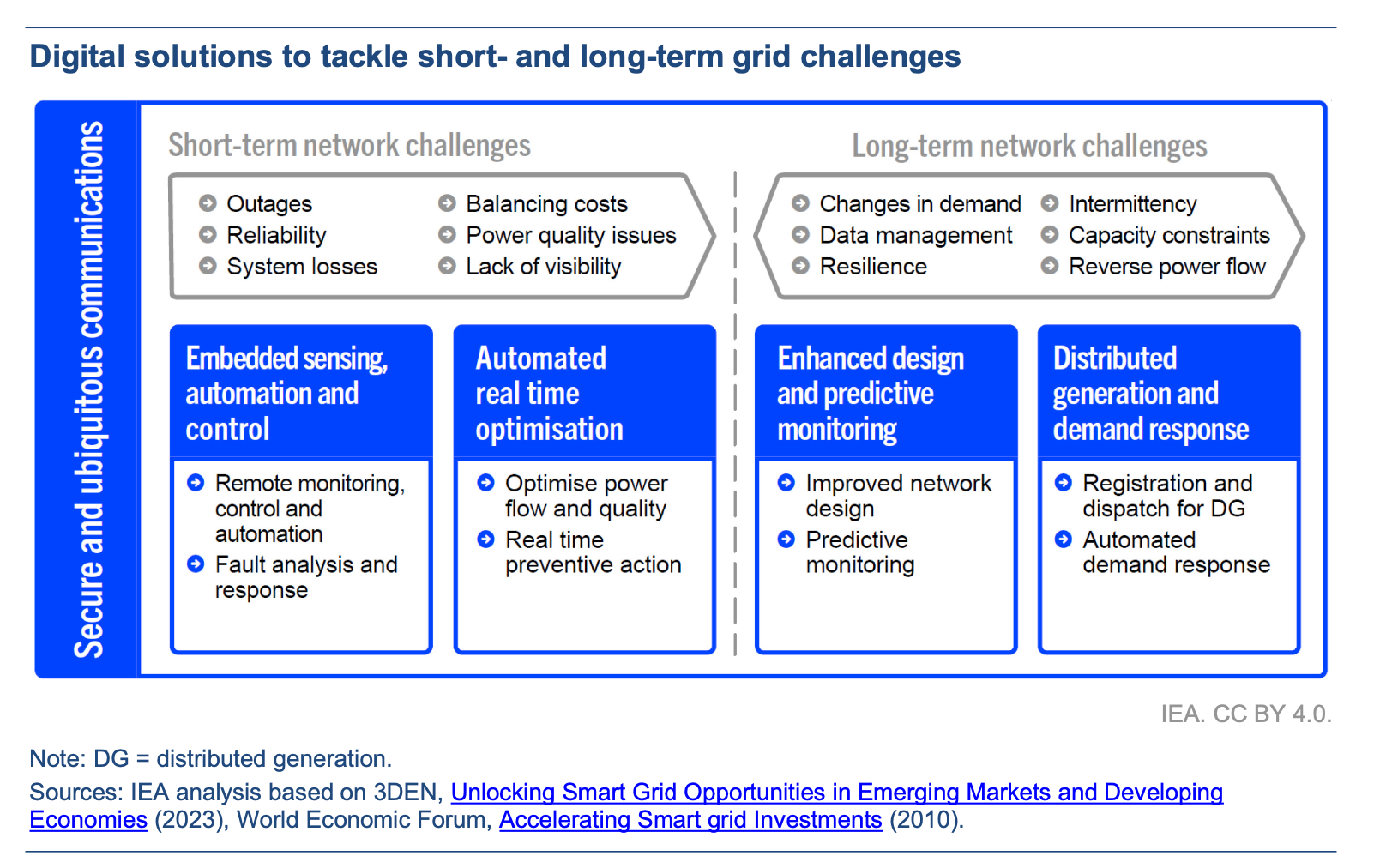

3. Digitalization

Digital solutions are assuming a pivotal role in real-time monitoring and control of the grid. With the rising penetration of distributed generation from renewable sources, the direction of energy flows within the grid is becoming multidirectional and less predictable requiring new digital solutions. Digital & IOT Solutions, will also enable enhanced proactive and preventive maintenance.

4. Grid resilience amid increased climate risks

The Grids are exposed to the vagarities of nature, and amid the increasing frequency and intensity of extreme weather events, redundancies/buffers are required to be built in the system.

To Summarize

Grid infrastructure creation is a mega-trend backed by increasing energy consumption, with the consumption electrified using renewables.

Clean energy transitions need the grid of the future equipped with energy-efficient technologies, digitalized equipment, and processes. Digitalization and more distributed resources create an opportunity for smarter and more resilient grids while requiring them to operate more flexibly.

The decentralized nature of renewables needs the future grid to be more resilient to handle short-term variations and seasonal variations while also being capable of handling risks of extreme weather patterns emerging from climate change.

Microgrids and storage will complement the infrastructure, and build buffer capacities, and redundancies. Countries/regions will interconnect grids to increase resilience and derive economic benefits.Globally, a lot is required in this space.

PS: I will be doing a detailed post on Indian Power Sector. So stay tuned 🙂

References:

IEA, BP Energy Outlook Reports, JP Morgan Reports on Clean Energy, Siemens, ValueQuest

Invest in yourself…. be a learning machine

These communities have helped me a lot in learning the nuances of investing. Why not check them out? - Join the community of learners.

This Substack will never be paywalled. I don’t want to accept voluntary payments for future unknown work.

But if you got this far, chances are you find my writing valuable. So please spread the word! Sharing, liking, and commenting all help spread the word! 😀

Thanks for reading. Please do share your feedback.

Connect with me on Twitter: @pankajgarg_ciet

Disclaimer: I am not SEBI registered. The information provided here is for educational purposes only. This is not buy or sell advice. I will not be responsible for any of your profit/loss based on the above information. Consult your financial advisor before making any decisions.

Comprehensive

Excellent post !!

Power Value Chain is crystal clear to me now !!